Nike (NKE) Stock Looks Reasonable On Cash Flow But Stretched On Earnings

NIKE, Inc. Class B NKE | 0.00 |

NIKE’s stock has fallen sharply over the past few years, yet current checks suggest it now trades close to its estimated intrinsic value. This leaves investors weighing a steep share price decline against a valuation picture that looks more “about right” than clearly cheap.

- NIKE’s share price is down 72.2% over five years, which means today’s valuation is being assessed against a much lower base than in the past.

- Expectations that the turnaround can support future cash flows, set against execution risks around China weakness, wholesale resets and changing consumer demand, may be the main swing factors for how the stock is priced from here.

- On Simply Wall St’s broader checks NIKE scores 2 out of 6 for value, which points to a company that does not screen as a clear bargain on most metrics even if the Discounted Cash Flow (DCF) estimate sits close to the current share price.

The issue now is whether NIKE’s recent price weakness has already accounted for these risks or if the stock’s current level still leaves limited upside against its intrinsic value estimate.

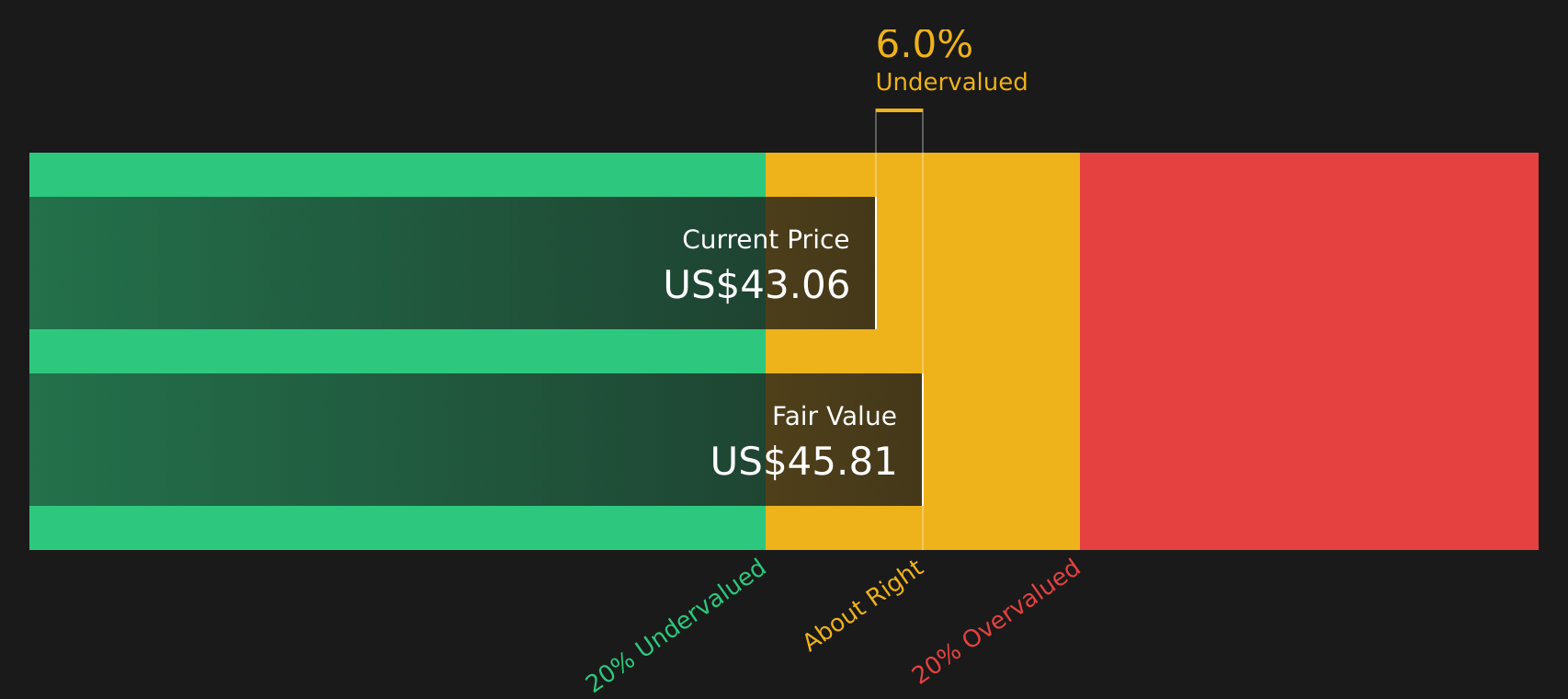

Is NIKE Fairly Priced on Cash Flow?

The Discounted Cash Flow (DCF) model here focuses on what NIKE can earn for shareholders over time. On this approach, NIKE’s latest twelve month free cash flow is about $1.0b, with the model assuming that cash flows recover rather than shrink over the long run. Those projections translate into an estimated intrinsic value of around $40.46 per share.

With the current share price sitting only about 1.5% above that DCF estimate, NIKE screens as roughly in line with its cash flow valuation rather than clearly cheap or expensive. Recent downgrades that flag slower progress in the turnaround and execution issues in wholesale and China help explain why the market is reluctant to price the stock much above the modelled intrinsic value.

Overall, NIKE’s stock currently looks roughly fairly valued relative to this DCF-based intrinsic value estimate.

NIKE is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

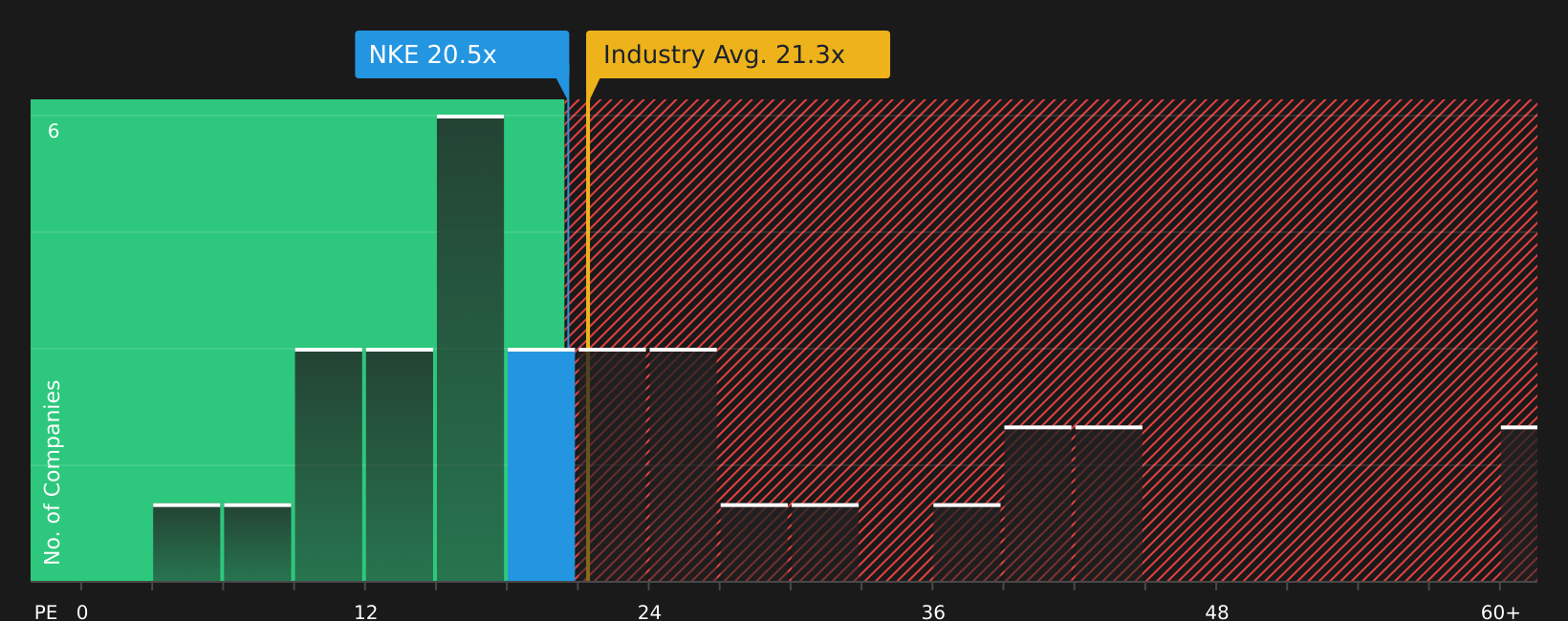

Where Does NIKE Sit on Earnings?

The P/E ratio is a useful way to think about what you are paying for each dollar of NIKE’s earnings, which suits a mature, profitable consumer brand like NIKE.

NIKE currently trades on a P/E of about 27.0x, very close to the peer average of 27.8x and above the broader luxury industry average of 22.1x. On Simply Wall St’s model, a more tailored “fair” P/E for NIKE, based on its size, margins and risk profile, sits at around 29.4x, which is modestly higher than where the stock trades today.

This points to a stock that neither stands out as a bargain nor as stretched on earnings compared with similar companies. The recent downgrades and ongoing turnaround questions appear to be broadly reflected in the current P/E without pushing it to an extreme discount or premium.

Put together, NIKE’s earnings multiple looks broadly in line with what the model suggests is a fair P/E, so the stock appears roughly fairly valued on this measure.

The NIKE Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for NIKE pick up where the valuation checks leave off, by spelling out what would need to happen to NIKE's growth, margins and earnings for the stock to be worth materially more or less than today. Each one treats fair value as a thesis about NIKE's business that can be tracked over time, rather than a one off number, and they sit on Simply Wall St's Community page for you to assess.

Community views on NIKE sit far apart, with one camp seeing reset products and brand work as a foundation for resilience, and the other focused on slower progress and external risks.

Bull case: 32% undervalued

"Nike is accelerating the transition of its product portfolio, aiming for sport performance dimensions to drive growth, decrease reliance on declining lines, and positively impact revenue..."

Bear case: 73% overvalued

"The company is losing brand heat and cultural relevance, especially among Gen Z and younger consumers who are increasingly favoring challenger brands, fast fashion, and hyperlocal or sustainability-focused labels..."

Do you think there's more to the story for NIKE? Head over to our Community to see what others are saying!

The Bottom Line

For NIKE, the Discounted Cash Flow (DCF) intrinsic value and the current P/E both point to a stock that is priced about right rather than clearly undervalued or overvalued. The broader checks are weak for value hunters, so anyone hoping for an easy bargain case is likely to be disappointed. From here, what matters most is whether NIKE can execute on its turnaround in China and wholesale, and keep consumer demand engaged so that current expectations for cash flows and earnings do not slip and force a rethink of today’s "roughly fair" pricing.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.