Nvidia (NVDA) Stock After New SharonAI Data Center Deal Is The AI Leader Still Undervalued

NVIDIA Corporation NVDA | 0.00 |

NVIDIA (NVDA) just signed a six year compute collaboration with SharonAI Holdings to support 72 megawatts of new AI data center capacity in Australia, using its DSX AI factory design and Grace Blackwell GB300 GPUs.

NVIDIA’s recent string of AI factory and data center agreements has kept the story in focus even as momentum has cooled. The 30 day share price return is down 8.93%, but the 5 year total shareholder return is above 10x, and the latest 90 day share price return of 11.99% points to interest that has eased rather than disappeared.

If you want to see what else is building out AI infrastructure alongside NVIDIA, now is a good time to scan the market using our AI infrastructure stocks screener, starting with 48 AI infrastructure stocks.

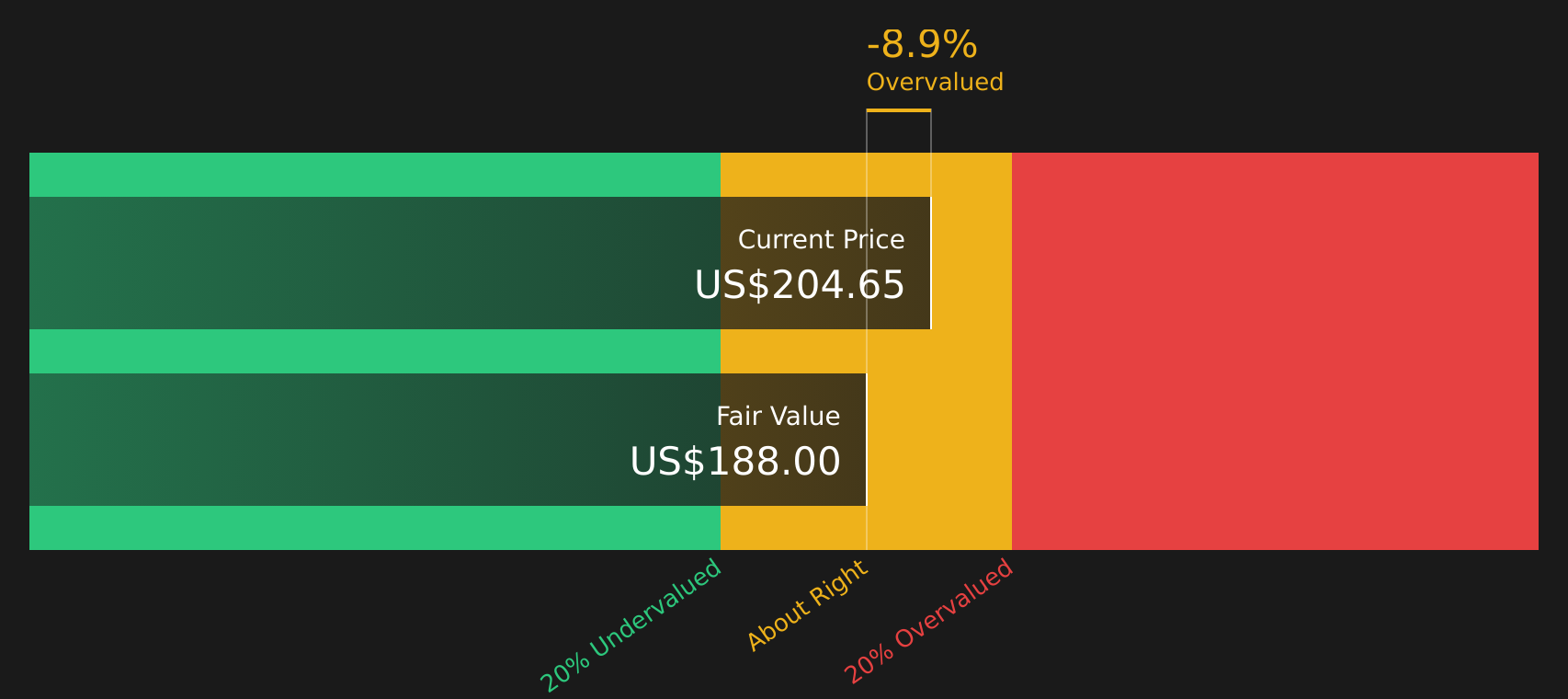

Valuation is where opinions split. NVIDIA trades around $205.19, the 30 day return has declined 8.93% while the 5 year total shareholder return is above 10x and analysts see about 46% upside to a US$298.93 target. This raises the question: is this a genuine opportunity, or is the market already paying up for years of AI factory growth to come?

Most Popular Narrative: 39.6% Undervalued

On the most followed narrative, NVIDIA’s fair value of $339.90 sits well above the last close of $205.19, which naturally pulls attention to the assumptions behind that gap.

$400b annual revenue assumes Nvidia continues to be dominant in GPU design and AI software stack. Successful competition from AMD, Intel, or a Chinese firm could undermine this.

Uptake of an open-source, cheaper, or better platform than Nvidia's CUDA would heavily undermine Nvidia's moat and enable any sizeable firm to directly engage semiconductor manufacturers, such as TSMC, to produce their own chips, stealing away Nvidia's high margin products (similar to what Apple did with its M-Series chips).

The narrative, according to KiwiInvest, leans on very high AI data center revenue, premium margins and a future earnings multiple that assumes this dominance holds. Want to see which specific growth, margin and valuation levers are doing the heavy lifting in that $339.90 figure, and how they stack against today’s $205.19 share price?

Result: Fair Value of $339.90 (UNDERVALUED)

However, this depends on Nvidia maintaining its grip on AI GPUs and CUDA, while also avoiding tighter regulation or power constraints that could slow data center spending.

Another View: Cash Flows Paint A Tighter Picture

While the community narrative points to a $339.90 fair value and a 39.6% undervaluation, the SWS DCF model comes out more cautious. The model suggests that future cash flows indicate a value of $195.79, which is slightly below the current $205.19 price. Which signal do you consider more informative, the story or the cash flows?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out NVIDIA for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals on value and sentiment, this is a moment to look at the numbers yourself and act before views harden. To round out that picture, check the 4 key rewards and 2 important warning signs

Looking for more investment ideas?

If you stop with just one stock, you miss chances elsewhere, so widen the search now and let the data surface ideas you might overlook alone.

- Spot overlooked value by scanning 44 high quality undervalued stocks that combine quality fundamentals with pricing that may not fully reflect their financial strength.

- Build a sturdier portfolio by focusing on solid balance sheet and fundamentals stocks screener (48 results) that pair healthier finances with more resilient business profiles.

- Get ahead of the crowd by checking the screener containing 20 high quality undiscovered gems that strong fundamentals highlight before attention fully arrives.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.