Oracle (NYSE:ORCL) Valuation Check After Strong Share Price Momentum And AI Infrastructure Narrative

Oracle Corporation ORCL | 0.00 |

Oracle (ORCL) is back in focus for investors after recent share price moves, with the stock now around $192 and a market value of about $552.4b. This has prompted fresh attention on its valuation.

Recent trading tells a story of strong momentum building in Oracle’s share price, with a 10.85% 1 month share price return, a 35.93% 3 month share price return, and a 5 year total shareholder return of 161.01%.

If Oracle’s recent move has you rethinking your tech exposure, this is also a good moment to look at other AI related opportunities using the 46 AI infrastructure stocks

With Oracle trading near $192 and sitting on a market value above $552.4b, solid recent returns and an indicated intrinsic discount raise the core question: is there still value on the table, or are markets already pricing in future growth?

Most Popular Narrative: 50.7% Undervalued

According to the most followed narrative for Oracle, a fair value of about $389.81 versus the last close at $192.08 points to a wide valuation gap that hinges on a very specific AI infrastructure story.

The story of Oracle’s transformation is a narrative of strategic repositioning that has culminated in the company emerging as an indispensable infrastructure partner for the world’s most demanding Artificial Intelligence (AI) workloads. This strategic shift, defined by massive infrastructure investment, a landmark partnership with OpenAI, and the rise of colossal superclusters, has driven an unprecedented surge in its contract backlog, fundamentally reshaping Oracle’s long-term growth trajectory and competitive landscape.

Want to see what turns that AI infrastructure story into a valuation nearly double today’s price? The narrative leans on aggressive revenue expansion, rising margins, and a future earnings profile more often associated with fast growing cloud leaders. Curious which specific growth levers and cash flow assumptions are doing the heavy lifting in that $389.81 figure? The full narrative lays out the exact blueprint behind that fair value call.

Result: Fair Value of $389.81 (UNDERVALUED)

However, this AI heavy narrative still hinges on Oracle executing huge data center build outs on time and on customers actually converting large contract commitments into durable usage.

Another View: What Earnings Multiples Are Saying

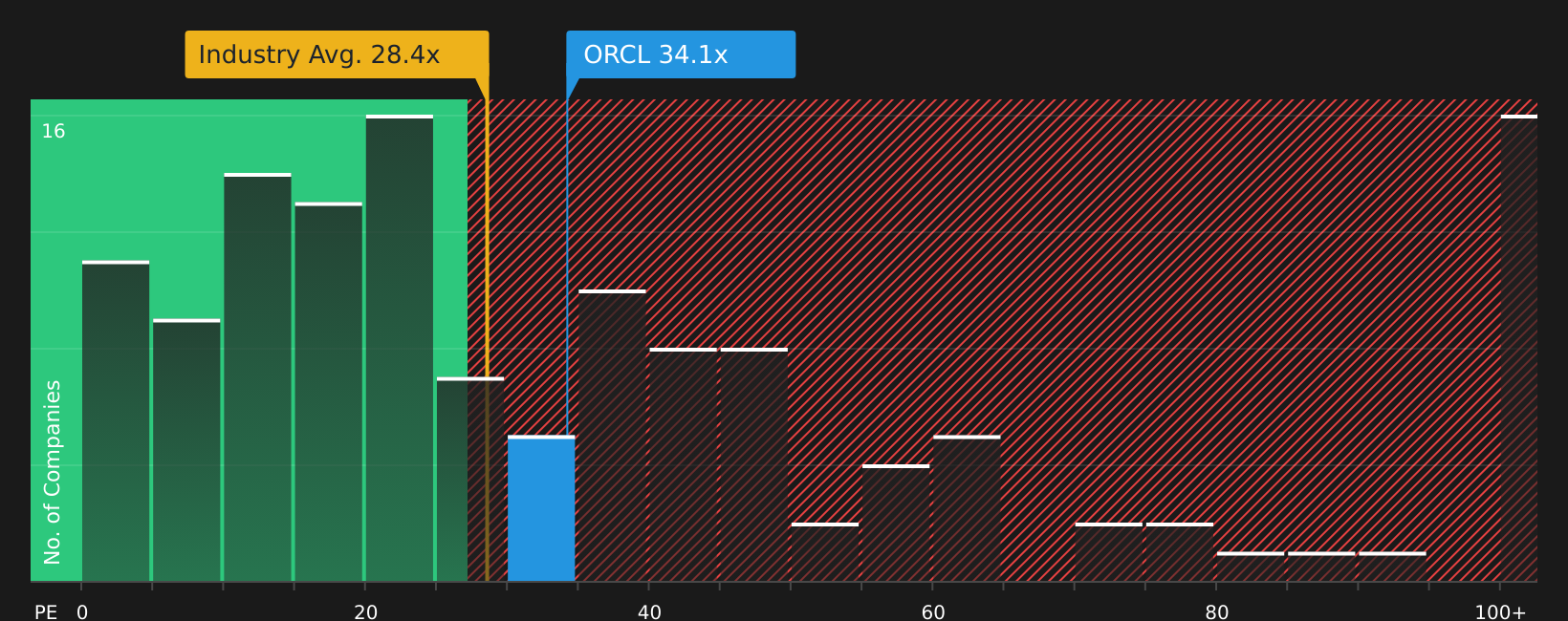

That $389.81 fair value hinges on an aggressive AI build out, but Oracle’s current P/E of 34.1x tells a more cautious story. It sits above the US Software industry at 28.4x, yet well below peers at 75x and a fair ratio of 61.3x, which flags both upside potential and valuation risk. Which signal do you trust more right now?

For a closer look at how this earnings multiple compares with what the fair ratio suggests the market could move toward, take a look at the See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

If this mix of enthusiasm and concern around Oracle leaves you on the fence, act while the data is fresh and weigh both sides using the 3 key rewards and 2 important warning signs.

Looking for more investment ideas?

Do not stop with a single stock. Give yourself options, compare different angles, and keep fresh ideas coming so you are not reacting after the move.

- Target resilient income by checking stocks that aim for reliable payouts using the 10 dividend fortresses.

- Hunt for strong businesses that the market may be overlooking by scanning the screener containing 21 high quality undiscovered gems.

- Prioritize capital protection first by reviewing companies with steadier risk profiles in the 67 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.