Piper Sandler (PIPR) Margin Improvement And 44.1% Earnings Growth Test Valuation Concerns

Piper Sandler Companies PIPR | 89.39 | +0.91% |

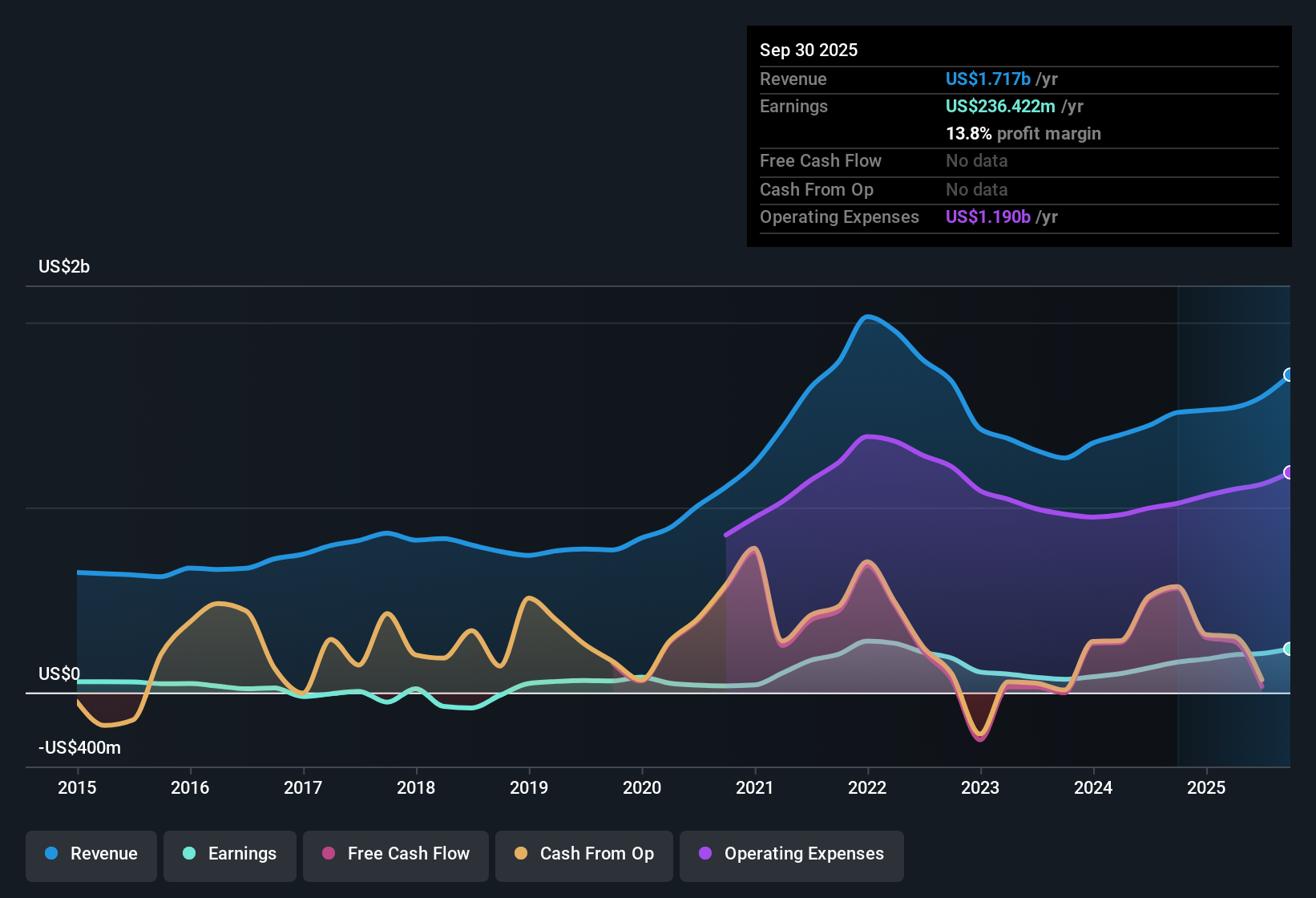

Piper Sandler Companies (PIPR) has put up another solid quarter, with Q3 FY 2025 revenue of US$479.3 million and basic EPS of US$3.61, supported by trailing twelve month EPS of US$14.36 on revenue of US$1.7 billion. Over the past year, the firm has seen total revenue move from US$1.4 billion on trailing EPS of US$8.64 at Q2 2024 to US$1.7 billion on EPS of US$14.36 at Q3 2025, alongside one year earnings growth of 44.1%. With net profit margins improving to 13.8% from 10.8% over the last 12 months, the latest results point to a business that is currently converting a larger share of revenue into profit.

See our full analysis for Piper Sandler Companies.With the headline numbers on the table, the next step is to see how this earnings picture lines up with the widely followed narratives around Piper Sandler, where some long held views may be confirmed while others get tested against the data.

44.1% earnings growth versus 3.3% long run

- Over the last 12 months, earnings grew 44.1% while the five year compound annual earnings growth rate was 3.3%, so the recent period looks much stronger than the longer run trend.

- What stands out for a more bullish view is that this faster phase in earnings is backed by trailing twelve month net income of US$236.4 million on US$1.7b of revenue, compared with US$133.2 million on US$1.4b of revenue a year earlier. This heavily supports arguments that recent performance has been stronger than the five year pace.

- Trailing EPS moved from US$8.64 at Q2 2024 to US$14.36 at Q3 2025, which lines up with that 44.1% annual earnings growth figure.

- Across the last six quarters, quarterly net income ranged from US$34.8 million to US$69.1 million, so the current trailing outcome reflects several solid quarters rather than a single spike.

Margins at 13.8% versus 10.8% last year

- Net profit margin on a trailing basis is 13.8% on US$1.7b of revenue, compared with 10.8% a year earlier on US$1.4b. This ties the earnings growth to higher profitability on each dollar of revenue.

- Bulls often focus on margin strength and here the improvement from 10.8% to 13.8% sits alongside a trailing P/E of 27.3x, so while the higher profitability helps earnings quality, it also means investors are paying more for each dollar of those profits than the US Capital Markets industry average of 22.9x and a peer average of 8.7x.

- Trailing net income increased from US$133.2 million to US$236.4 million on the revenue base, which backs the idea that higher margins have been an important driver of the 44.1% earnings growth.

- The gap between the 13.8% margin now and 10.8% a year ago is one reason some investors might accept a premium P/E, even though the multiple is above both the industry and peer averages.

Strong trailing margins and earnings growth raise a common question for investors, and the community narratives can give you a feel for how others are weighing those numbers against valuation and risk in their own process. Curious how numbers become stories that shape markets? Explore Community Narratives

P/E of 27.3x and DCF fair value gap

- The shares trade on a trailing P/E of 27.3x compared with a US Capital Markets industry average of 22.9x and a peer average of 8.7x, while the current share price of US$364.38 sits well above a DCF fair value estimate of about US$64.32.

- Critics highlight these valuation markers and also point to a 1.59% dividend that is not well covered by free cash flow and recent insider selling, so the cautious view is that the premium multiple and the large gap to DCF fair value leave less room for disappointment even though trailing earnings growth and margins have improved.

- The ratio between the share price of US$364.38 and the DCF fair value of roughly US$64.32 implies the market price is several times that modelled value. This is often flagged in more bearish discussions.

- Weak free cash flow coverage of the 1.59% dividend and significant insider selling over the past three months are additional data points cautious investors may consider alongside the higher P/E.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Piper Sandler Companies's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

For all the strong earnings, Piper Sandler's trailing P/E of 27.3x, the large gap to DCF fair value and weak free cash flow dividend cover may leave some investors cautious.

If that rich valuation and tight cash cover make you uneasy, you might want to balance your watchlist with 53 high quality undervalued stocks to screen for stronger value based on current pricing.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.