Procter & Gamble (PG) Stock After Recent Weakness And Conflicting Fair Value Estimates

Procter & Gamble Company PG | 0.00 |

- If you are wondering whether Procter & Gamble stock at around US$148.34 offers good value for your portfolio, the answer depends on how you look at its valuation rather than just the headline price.

- The stock has gained 5.4% over the past week, 3.1% over the last 30 days and 4.6% year to date, while returns over the last year are down 6.5% and sit at 8.0% over 3 years and 25.7% over 5 years.

- Recent coverage has focused on how Procter & Gamble fits into broader conversations about consumer staples, pricing power and defensiveness, which helps frame the recent moves in the share price. Investors are weighing how consistent demand for everyday products might balance against changing expectations for returns from large established companies.

- On Simply Wall St's valuation checks, Procter & Gamble scores 4 out of 6. This sets up a closer look at what different valuation approaches are saying about the stock today, and an even richer way of thinking about valuation that will be covered at the end of this article.

Approach 1: Procter & Gamble Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a stock could be worth by projecting the company’s future cash flows and discounting them back to today using a required rate of return.

For Procter & Gamble, the model used is a 2 Stage Free Cash Flow to Equity approach based on cash flow projections. The company’s latest twelve month free cash flow is about $15.6b. Analyst estimates run out part way through the forecast period, so Simply Wall St extrapolates further years to build a ten year view of free cash flow in dollars.

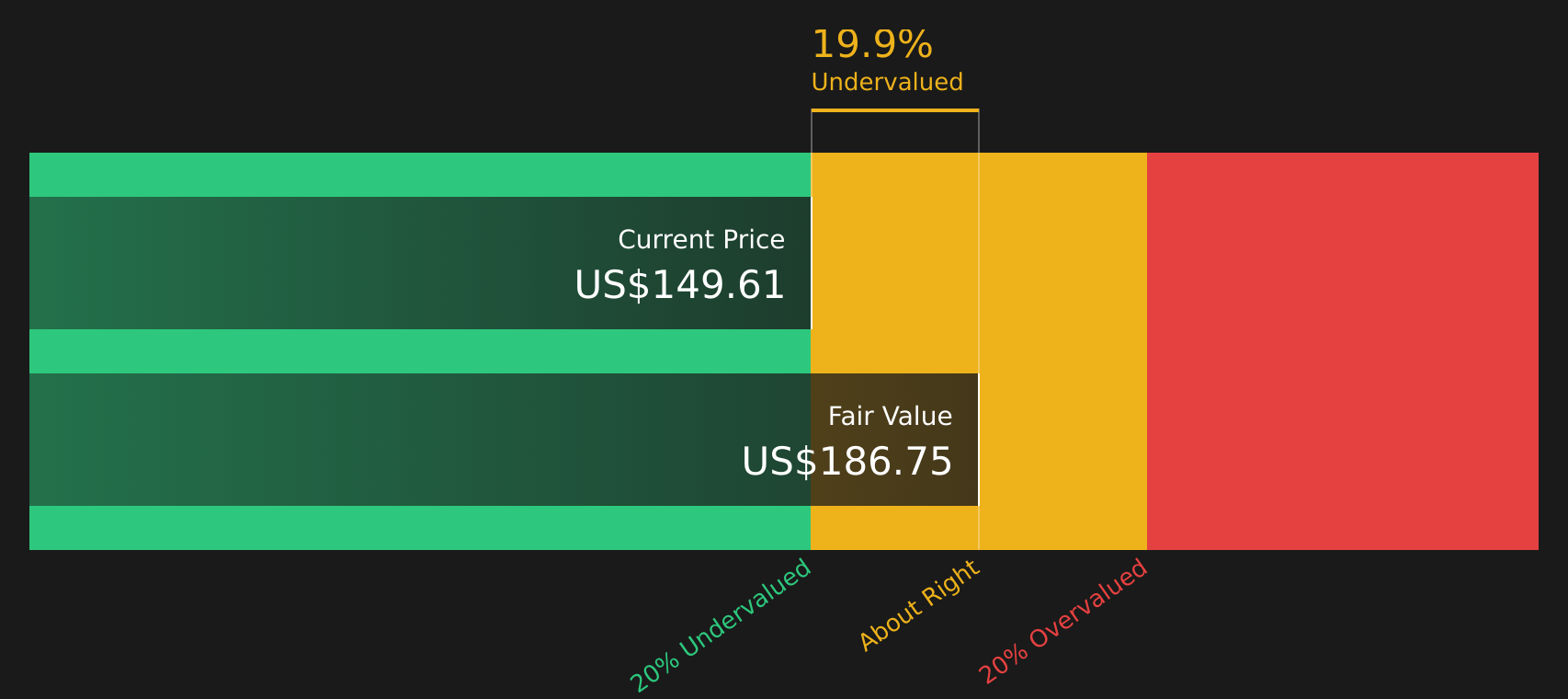

Across these projections, free cash flow in the tenth forecast year is modeled at around $21.3b, with each year discounted back to reflect the time value of money. Adding those discounted cash flows together and including a terminal value gives an estimated intrinsic value of about $186.75 per share.

Against a current share price around $148.34, this DCF output suggests the stock trades at roughly a 20.6% discount on this model alone.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Procter & Gamble is undervalued by 20.6%. Track this in your watchlist or portfolio, or discover 46 more high quality undervalued stocks.

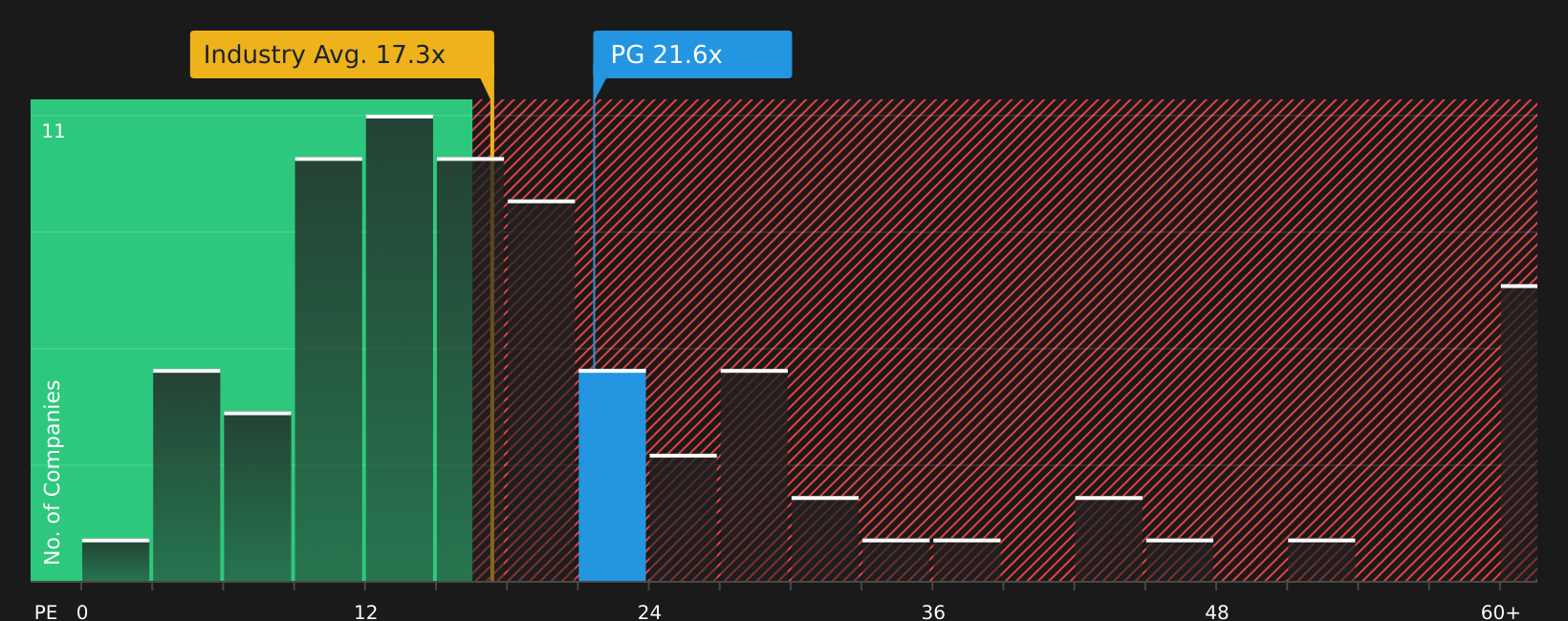

Approach 2: Procter & Gamble Price vs Earnings

The P/E ratio is a common way to value profitable companies because it links what you pay for the stock to what the business is currently earning. For investors, it is a quick gauge of how many dollars of price correspond to each dollar of earnings.

What counts as a “normal” or “fair” P/E often reflects how the market views a company’s growth potential and risks. Higher expected earnings growth or lower perceived risk can support a higher P/E, while slower growth or higher risk can justify a lower one.

Procter & Gamble currently trades on a P/E of about 21.16x, compared with an average of 25.24x for peers and around 16.82x for the broader Household Products industry. Simply Wall St’s proprietary “Fair Ratio” for Procter & Gamble is 22.42x. This Fair Ratio is an estimate of what the P/E might be when factors such as earnings growth, industry, profit margins, market cap and company specific risks are considered together.

Because the Fair Ratio blends these fundamentals, it can offer a more tailored benchmark than simple peer or industry comparisons. With the current P/E slightly below the Fair Ratio, the stock screens as mildly undervalued on this metric.

Result: UNDERVALUED

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Upgrade Your Decision Making: Choose your Procter & Gamble Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Meet Narratives, which let you spell out the story you believe about Procter & Gamble, link that story to specific forecasts for revenue, earnings and margins, and then turn those forecasts into a Fair Value that you can compare with today’s price to decide whether the stock looks attractive, stretched or somewhere in between.

On Simply Wall St’s Community page, Narratives are simple to use. They sit on top of familiar metrics and are updated automatically when new information such as earnings, news or guidance is added to the platform. This helps your Fair Value view stay aligned with the latest data without extra work from you.

For Procter & Gamble, one investor might build a Narrative around consumer wellness and brain health, using assumptions similar to the US$122.36 Fair Value shown in one community view. Another might focus on slower growth, cost of capital at 8.32% and a wide moat to arrive at a Fair Value closer to US$121.06. Putting these side by side with the current share price may help you decide whether your own story justifies holding back, adding, or waiting for a different price before acting.

For Procter & Gamble, however, we will make it really easy for you with previews of two leading Procter & Gamble Narratives:

Fair value: US$150.00 per share

Implied discount to this fair value: about 1.1% below the narrative fair value based on the last close of US$148.34

Revenue growth assumption: 8.09%

- The author sees recent share price weakness and tariff related uncertainty as pushing the stock toward oversold territory, with Simply Wall St fair value at US$185.05 and the author’s own estimate at around US$150.

- The narrative highlights a wide range of globally recognised consumer brands, high gross and net margins around 50% and 18 to 19% respectively, and a product set focused on non discretionary spending.

- It flags insider selling and higher leverage, with debt to equity around 67%, but notes strong interest coverage near 51 times and frames the stock as one to watch for signs of stabilising price action or renewed insider buying.

Fair value: US$121.06 per share

Implied premium to this fair value: about 22.5% above the narrative fair value based on the last close of US$148.34

Revenue growth assumption: 3.32%

- This narrative scores Procter & Gamble 9.5 out of 17 on key metrics, pointing to a projected operating margin of 25.16%, a last 5 year ROIC of 17.20% against an 8.32% cost of capital, and a wide moat with low uncertainty.

- The author uses a blend of approaches including DDM, DCF, historical multiples and EPS growth, with several Monte Carlo simulations indicating the current price screens above the upper valuation ranges in some models.

- While several historical multiples and the dividend yield suggest undervaluation, the weighted conclusion is a fair value of US$121.06, which leads the author to view the stock as trading above their estimate of intrinsic value at recent prices.

Together, these Narratives show how two informed investors can look at the same set of brands, margins and balance sheet data yet arrive at very different fair values, which is exactly the kind of tension that can help you refine your own view of Procter & Gamble.

Do you think there's more to the story for Procter & Gamble? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.