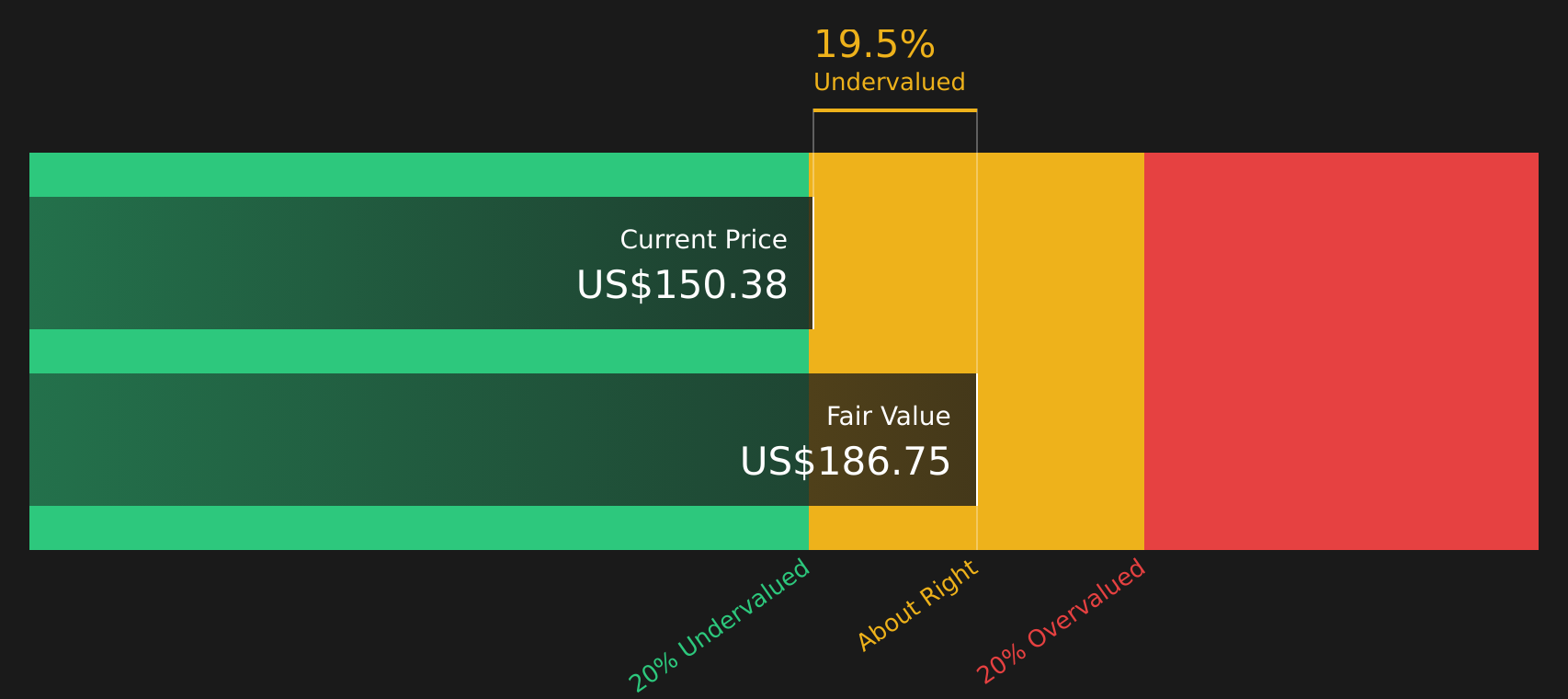

Procter & Gamble (PG) Stock Could Be 19.5% Undervalued After Broad Based Growth

Procter & Gamble Company PG | 0.00 |

Procter & Gamble (PG) is back in the spotlight after reporting broad-based growth across core brands like Tide, Pampers, and Gillette, along with fresh marketing moves and continued dividend and buyback activity.

Despite the fresh product launches and media partnerships, Procter & Gamble’s recent share price return has been steady rather than dramatic, with a 30-day share price return of 4.11% and a 90-day share price return of 4.44%, while the 1-year total shareholder return has declined 2.75%. This suggests modest near term momentum alongside a more subdued longer term picture.

If Procter & Gamble’s steady profile has you thinking about what else could be in your portfolio, this is a good moment to broaden your search and uncover 20 top founder-led companies

With Procter & Gamble posting broad-based growth, trading at about an 8.7% discount to its analyst price target and an estimated 19.5% intrinsic discount, you have to ask: Is there still value here, or is the market already pricing in future growth?

Most Popular Narrative: 24.2% Overvalued

The most followed narrative on Procter & Gamble pegs fair value at $121.06, well below the recent $150.38 close, so the story hinges on quality versus price.

Procter & Gamble despite being within a very competitive industry still has some competitive advantages shown on its higher operating margin above the ~20% mark and the Morning Star Wide Moat. Also the fact that the ROIC is double the Cost of Capital means its capital allocation is being well managed.

The narrative leans heavily on rich margins, strong returns on invested capital and a wide moat, then tests those strengths against slower revenue growth and conservative future profit estimates.

Result: Fair Value of $121.06 (OVERVALUED)

However, this overvaluation call on Procter & Gamble could be challenged if its wide moat supports stronger pricing power than expected or if capital returns outpace current assumptions.

Another View On Procter & Gamble’s Valuation

While the user narrative points to Procter & Gamble being about 24.2% overvalued with a fair value of $121.06, the SWS DCF model tells a different story, with a future cash flow value of $186.75 and an implied 19.5% discount at the current $150.38 share price. Which set of assumptions do you find more convincing?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Procter & Gamble for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 45 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Seeing mixed sentiment around Procter & Gamble’s valuation and outlook, it makes sense to move quickly, test the assumptions against the data, and weigh both sides using the 4 key rewards and 1 important warning sign

Looking for more investment ideas beyond Procter & Gamble?

If Procter & Gamble has sharpened your focus on quality, do not stop there. Keep building a watchlist that fits your goals before the next opportunity slips past.

- Target dependable value by scanning companies that currently screen as 45 high quality undervalued stocks and see which ones align with your return expectations.

- Prioritise resilience by reviewing 65 resilient stocks with low risk scores that may better match a cautious or income focused approach.

- Hunt for overlooked potential by running the screener containing 19 high quality undiscovered gems and spotting stocks that are not yet crowded trades.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.