Procter & Gamble (PG) Stock Still Looks Below Fair Value Today

Procter & Gamble Company PG | 0.00 |

Procter & Gamble stock has delivered an 18.8% total return over the past 5 years, yet the current checks suggest the market price may still sit below an intrinsic value estimate based on a Discounted Cash Flow (DCF) approach and supported by earnings multiples.

- Over 5 years, a total return of 18.8% points to steady wealth creation, rather than the kind of surge that often leaves a clear valuation premium.

- Recent commentary around dividend resilience and modest organic growth suggests stable cash generation can support valuation. At the same time, any slowdown in demand for everyday products may cap how much investors are willing to pay for that stability.

- On Simply Wall St's broader checks, Procter & Gamble screens as a mixed case, with 4 out of 6 valuation tests indicating the stock leans toward undervalued rather than clearly expensive.

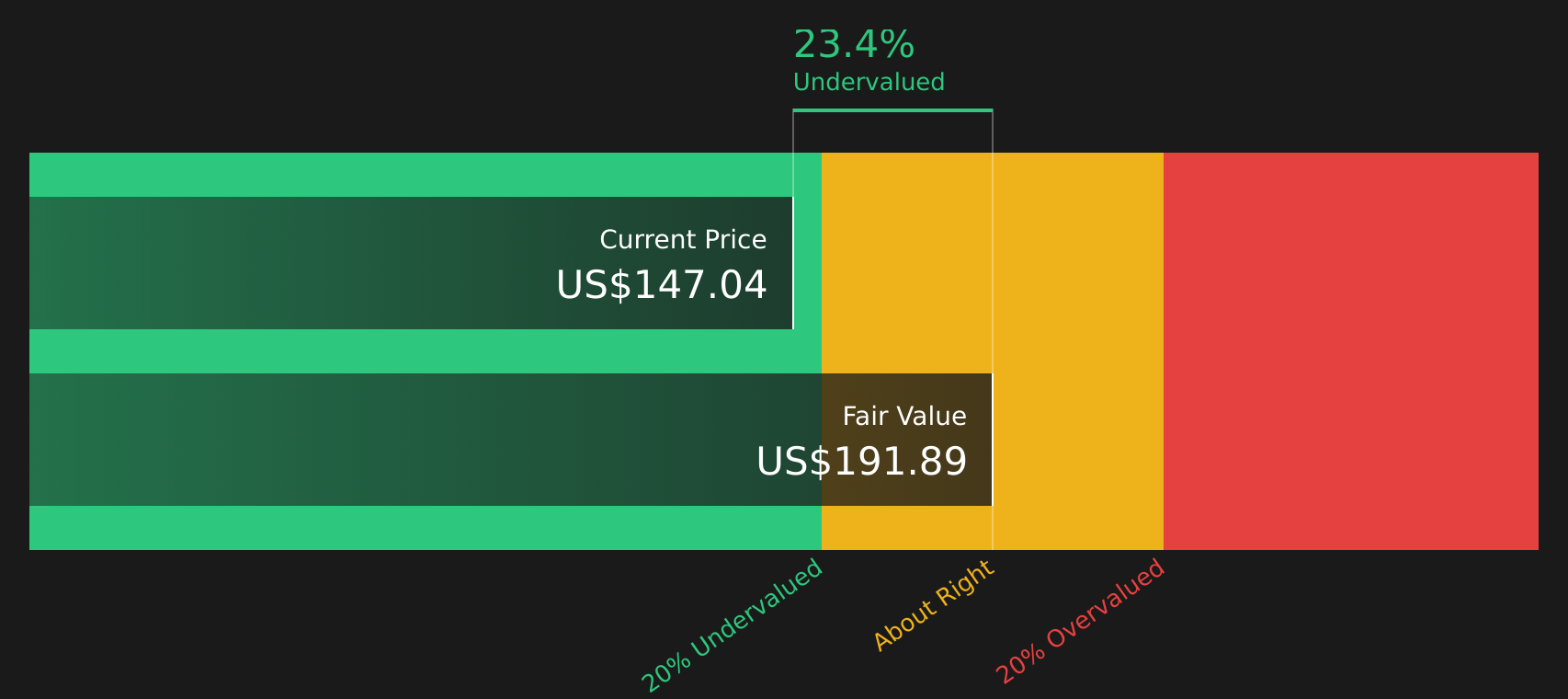

The issue now is whether Procter & Gamble's current share price of US$147.04 properly reflects its intrinsic value, or if the stock still offers a valuation cushion for long term investors.

Is Procter & Gamble Still Cheap on Cash Flow?

The Discounted Cash Flow (DCF) model used here is built on cash flow projections rather than near term earnings moves. For Procter & Gamble, the latest twelve month free cash flow is about $15.6b, and the 2 Stage Free Cash Flow to Equity model assumes these cash flows keep growing from this base, rather than shrinking or requiring a turnaround.

On that basis, Procter & Gamble's intrinsic value is estimated at about $191.89 per share, compared with the current share price of $147.04, implying the stock screens as roughly 23.4% undervalued. The recent focus on steady dividend capacity and modest organic growth, alongside earnings beats in recent quarters, is one reason a cash flow based model still supports a higher valuation, even as demand expectations remain restrained.

Overall, the DCF workup indicates Procter & Gamble stock currently appears undervalued relative to the cash flows analysts expect it to generate.

Our Discounted Cash Flow (DCF) analysis suggests Procter & Gamble is undervalued by 23.4%. Track this in your watchlist or portfolio, or discover 44 more high quality undervalued stocks.

Is Procter & Gamble a Bargain on Earnings?

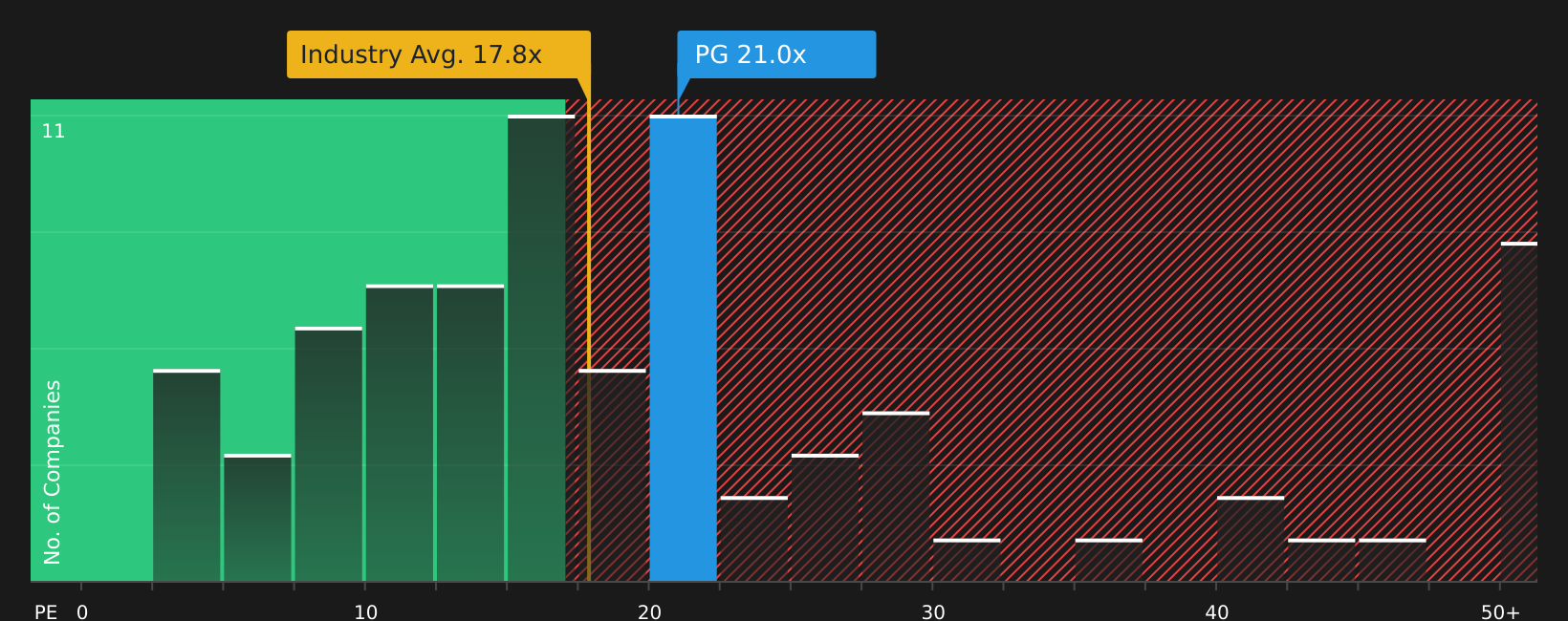

The P/E ratio is a useful yardstick for Procter & Gamble because earnings remain a central focus for income oriented investors watching both profits and dividends. Procter & Gamble currently trades on a P/E of about 21.0x, which sits below the Household Products industry average of roughly 17.6x and also below a peer group average of about 25.9x.

Simply Wall St's fair P/E estimate for Procter & Gamble is about 25.0x, reflecting what investors might expect to pay given its size, margins, and risk profile. Against that yardstick, the current multiple implies the stock trades at a discount to where this model suggests it could sit, even though the wider peer group commands an even higher average multiple.

On this P/E yardstick, Procter & Gamble stock appears undervalued relative to the earnings multiple implied by the fair value model.

The Procter & Gamble Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Procter & Gamble pick up where this valuation gap leaves off. They outline how different paths for Procter & Gamble's growth, margins and earnings could justify a stock price that is meaningfully higher or lower than today, and they sit on the company's Community page. Each one links its number to a clear view on how growth, profitability and key risks might evolve, giving you a reference point to revisit as new information comes through.

Community views on Procter & Gamble sit far apart, with some investors seeing a resilient compounder and others flagging valuation risk.

Bull case: roughly fairly valued

"PG operates with a gross margin around 50% and a net margin near 18 to 19%, indicating an efficient operation with significant safety buffers should consumer behaviour shift…"

Bear case: 21% overvalued

"From these simulations we can extrapolate that there''s more than 90% probability that the stock is overvalued at the current price…"

Do you think there's more to the story for Procter & Gamble? Head over to our Community to see what others are saying!

The Bottom Line

For Procter & Gamble, both the Discounted Cash Flow (DCF) intrinsic value estimate and the earnings multiple view point in the same direction, suggesting the stock screens as undervalued rather than stretched. The broader checks are mixed, so the gap between price and intrinsic value is not a definitive signal, but it does indicate some valuation support if current assumptions hold.

The core split between bulls and bears now centers on whether Procter & Gamble can sustain its margins and steady cash generation without demand for everyday products softening enough to justify a lower, more cautious multiple.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.