Research Digest | Are US Stocks Primed for Another July Rally? Essential Catalysts to Watch

PowerShares QQQ Trust,Series 1 QQQ | 0.00 | |

VanEck Vectors Semiconductor ETF SMH | 0.00 | |

Microsoft Corporation MSFT | 0.00 | |

Apple Inc. AAPL | 0.00 | |

NVIDIA Corporation NVDA | 0.00 |

Subscribe to The Value Anchor Topic / The Trend Catcher Topic —unlock the full historical archive and never miss a weekly pick again.

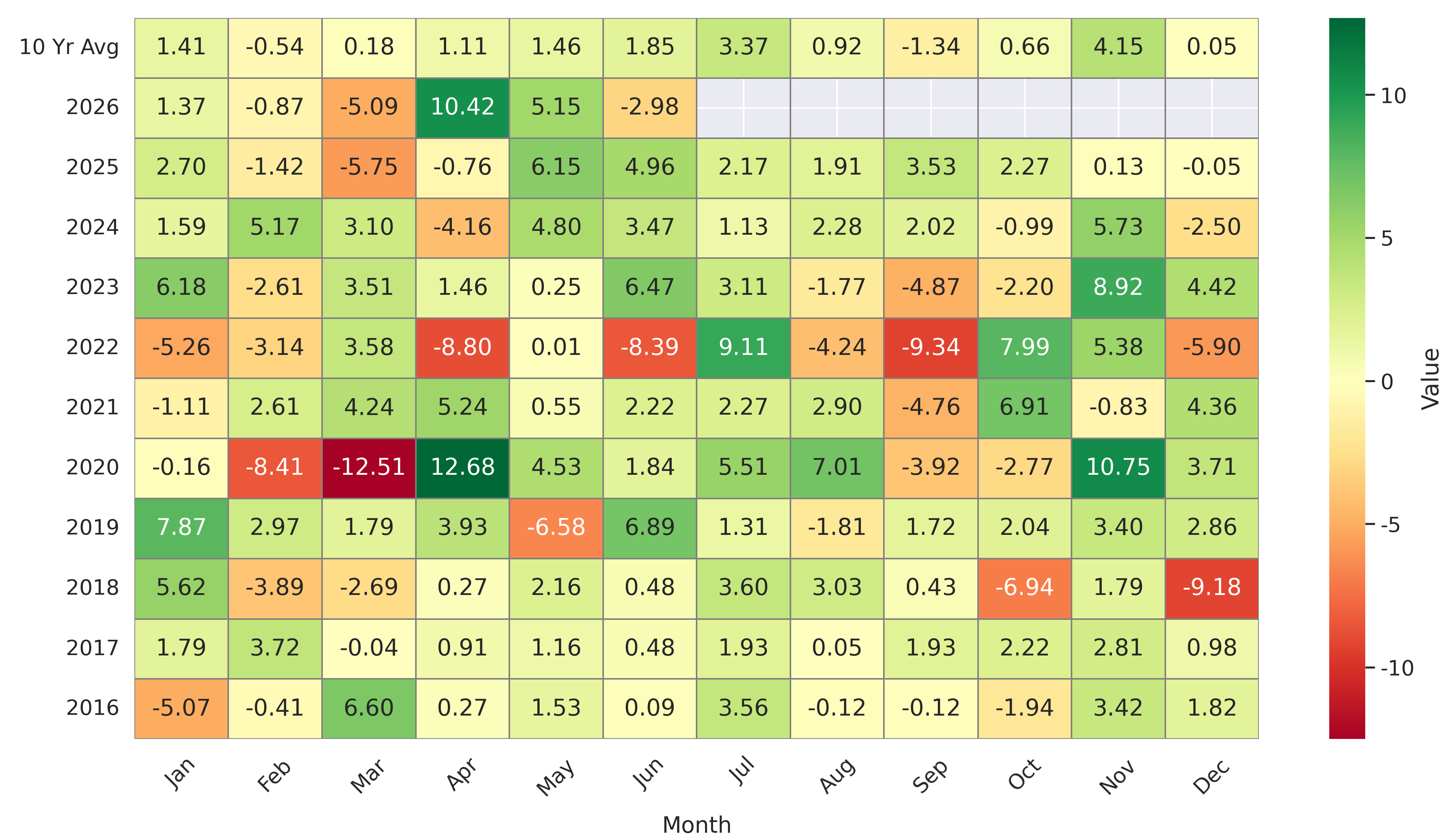

- June Review: US equities saw divergent performance driven by Fed policy anxieties and geopolitical shifts. The Nasdaq (-6%) and S&P 500 (-3%) pulled back, while the Dow Jones (+2%) hit record highs amid easing geopolitical tensions and value rotation.

- July Seasonality Tailwind: Short-term pullbacks may offer optimal risk-reward entry points. Historically, July is one of the most stable months for the S&P 500, boasting a 100% win rate over the past decade with an average gain of 3.37%—demonstrating resilience even during the 2020 pandemic and the 2022 rate-hike cycle.

Macro Strategy & Institutional Views

Consensus among major institutions points to increased volatility but a positive underlying trend supported by robust earnings:

- Goldman Sachs: The market remains in "buy-the-dip" mode, underpinned by strong corporate earnings and healthy liquidity. However, extreme market crowding poses a volatility risk.

- Morgan Stanley: Fundamental earnings growth remains the primary upside driver. While short-term liquidity may tighten, risk appetite over a 6–12 month horizon remains strong.

- Bank of America: The "AI Trade" is not over but is entering Phase II. Capital is rotating from crowded mega-caps (Magnificent 7) into small-caps, cyclicals, and emerging markets. (Warning: A drop in MAGS ETF below $60 or AUD/JPY below 110 could trigger summer risk-aversion).

Sector Focus & Capital Rotation

Funds are rapidly rotating out of big tech into semiconductors, memory, and defensive/cyclical plays.

- AI & Memory Storage: The storage cycle is outperforming expectations. HBM (High Bandwidth Memory) growth is projected at 80% through 2027, alongside strong DRAM pricing. SK Hynix’s upcoming Nasdaq ADR listing (July 10) could trigger a sector re-rating.

- Cloud/Compute Pricing: AWS is raising ML GPU instance prices by 20% on July 1. Market reactions will be a key indicator of computing power supply-demand tightness.

- Tactical Plays: Favorable setups are seen in eCommerce Cloud (oversold, strong fundamentals), specific AIDC hardware, and short-term event-driven plays like commercial aerospace. Caution is advised for heavily crowded optical communication stocks breaking below moving averages.

Key July Test: CSP Earnings & CapEx

Fund managers emphasize maintaining core equity exposure in July but warn against chasing overextended rallies. The most critical test this month will be the Cloud Service Provider (CSP) earnings season.

- The CapEx & ROI Dilemma: Investors will heavily scrutinize capital expenditure growth and the Return on Investment (ROI) of AI infrastructure. The market's stance on CapEx is strict: "too low is bearish, but too fast is alarming." Vague ROI guidance from tech giants represents the primary risk for this earnings season.

Key Dates & Watchlist (EST)

Macro & Fed Policy:

- July 1-2: ISM Manufacturing PMI, ADP Employment, & Non-Farm Payrolls (Crucial for gauging if the economy is overheating).

- July 8: FOMC Meeting Minutes.

- July 14-16: June CPI, PPI, and Retail Sales (Inflation basic fundamentals).

- July 29: FOMC Rate Decision & Warsh Press Conference.

- July 30: PCE Price Index.

Corporate & Market Events:

- July 3: US Markets closed (Independence Day observance).

- July 10: SK Hynix ADR Nasdaq Listing.

- July 14: US Bank Earnings Kickoff (GS, C, JPM, BAC).

- July 22-23: AMD "Advancing AI" Event.

Key Investment Themes & Hedging Tools for July

1. Big Tech & The AI Trade (Earnings Season Catalysts):

Tech giants with robust earnings visibility tend to rebound fastest after a pullback.

- ETFs to Watch: PowerShares QQQ Trust,Series 1(QQQ.US), VanEck Vectors Semiconductor ETF(SMH.US).

- Key Tickers: Microsoft Corporation(MSFT.US), Apple Inc.(AAPL.US), NVIDIA Corporation(NVDA.US), Alphabet Inc. Class C(GOOG.US)

2. S&P 500 (Core Broad Market & Downside Protection):

To navigate macroeconomic noise and a sustained high-interest-rate environment, balancing core long positions with inverse ETFs acts as an effective "insurance policy" to smooth out portfolio volatility.

- Long (Core Holding): ETF-S&P 500(SPY.US) or Vanguard S&P 500 Etf(VOO.US)

- Short/Hedge (Tail Risk Protection): ProShares Short S&P500 (Short S&P 500 Proshares(SH.US), 1x Inverse), ProShares UltraShort S&P500 (Ultrashort S&P 500 Proshares(SDS.US), 2x Inverse)

3. Russell 2000 (Tactical Short in a "Higher-for-Longer" Environment):

Without the relief of rate cuts, highly leveraged small-cap stocks that rely heavily on financing face the most severe fundamental pressure. If a broader market correction occurs, small caps are likely to lead the decline.

- Short Play (Tactical Hedging against High Rates): ProShares Short Russell2000 (Short Russell 2000 Proshares(RWM.US), 1x Inverse), Direxion Daily Small Cap Bear 3X Shares (Daily Small Cap Bear 3x Shares (TZA.US))

(Disclaimer: The tickers and strategies mentioned above are for informational and observational purposes only and do not constitute specific financial advice.)