Research Digest | Average 25% Pullback in Leaders — Has Storage Peaked? Morgan Stanley Offers 3 Key Metrics to Watch

Morgan Stanley MS | 0.00 | |

Micron Technology, Inc. MU | 0.00 | |

Sandisk Corporation SNDK | 0.00 | |

Western Digital Corporation WDC | 0.00 | |

Seagate Technology Holdings PLC STX | 0.00 |

Storage Stocks Pull Back as Peak Debate Intensifies

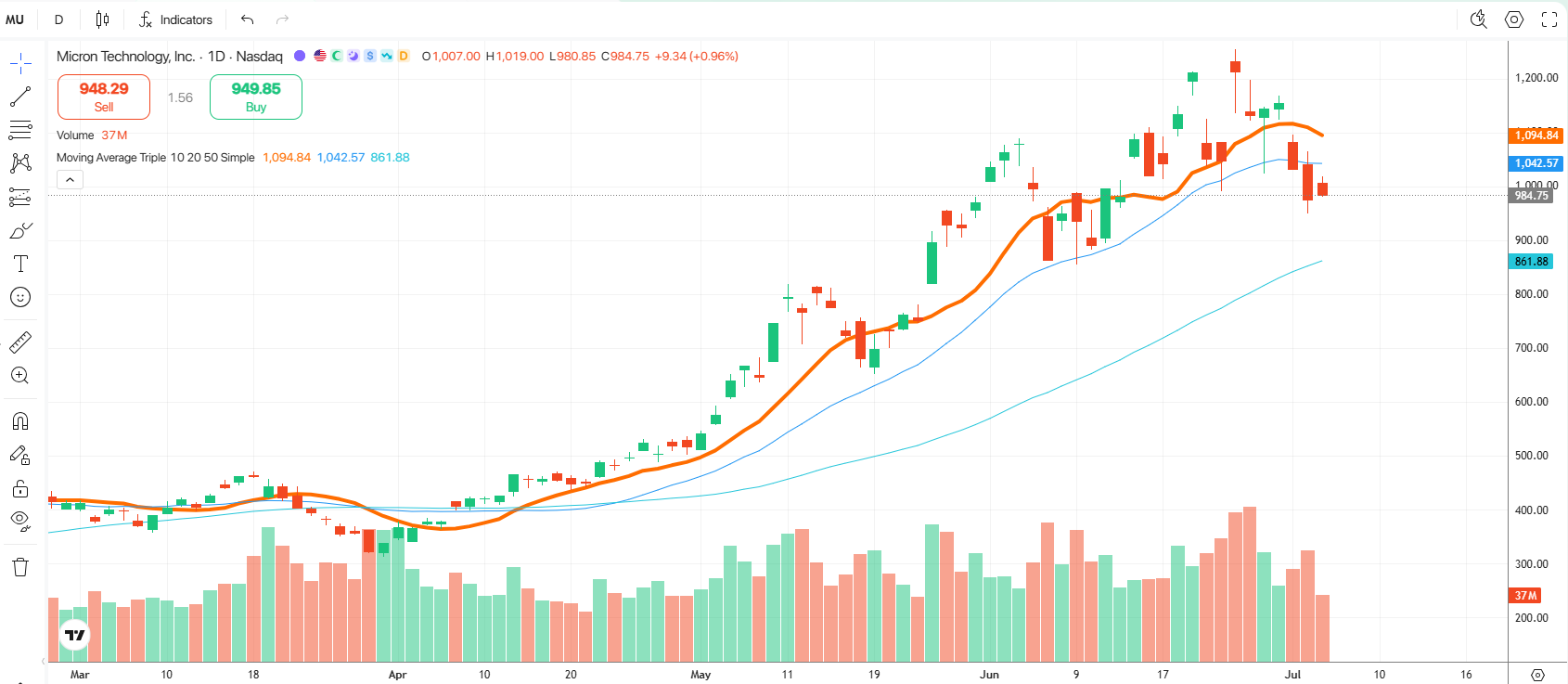

U.S. memory chip stocks have extended recent declines, with Micron Technology, Inc.(MU.US) down over 20% from its recent high, while Sandisk Corporation(SNDK.US) and Western Digital Corporation(WDC.US) have shed more than 25%. The sharp pullback has fueled growing market debate over whether the storage sector has peaked, after months of AI-driven gains.

Subscribe to Our The Trend Catcher Topic / The Value Anchor Topic Topics — Stay Tuned for More Trading Opportunities

Morgan Stanley warns the memory chip industry is nearing its "peak rate of change," with DRAM price gains narrowing, inventory improvement flattening, and EPS revision breadth topping. Near-term headwinds include concentrated positioning, higher volatility, and sector rotation pressure. Long-term outlook remains positive, with 2027 earnings growth projected at 35–40%. Key catalyst: whether hyperscalers sustain capex guidance.

The global memory chip industry is approaching a "peak rate of change" (Peak rate of change), but this does not signal the end of the cycle.

In a research report dated July 6, the core debates currently surrounding the memory chip market include: whether the price hike cycle has peaked, why Long-Term Agreements (LTAs) have failed to drive valuation reratings, and whether this is a cyclical top or a mid-bull market correction. The core conclusion of the report can be summarized in one sentence: The rate of change in price increases is peaking, but the cycle itself is not over.

As the largest AI compute buyers are reportedly starting to sell idle capacity, and enterprise demand for "token minimization" intensifies, the upward momentum of the memory sector is fading.

This implies that ahead of the upcoming earnings season, related stocks will face short-term price weakness and extreme volatility. The current market is highly crowded, and capital is preparing to rotate into laggard sectors. The bottom-line recommendation is: Remain bullish in the long term (with earnings projected to grow 35–40% by 2027), but beware of short-term pullbacks.

Three Core Debates: What is the Market Arguing About?

Three recurring debates from investor conversations over the past week serve as a key framework for understanding the current trajectory of the memory sector.

Debate 1: Is There a Genuine Compute Surplus?

An unverified rumor has circulated that one of the largest capex spenders in the AI space reportedly has excess compute capacity available for sale. Bears interpret this to mean that if hyperscalers have a compute surplus, the entire AI infrastructure buildout might be oversupplied. However, an alternative interpretation is that this is simply companies optimizing capital returns and monetizing idle infrastructure, which is not equivalent to a structural compute surplus.

The true moment of verification will be the Q2 2026 earnings season. If hyperscalers maintain or raise their capex guidance, it will be an excellent buying opportunity for memory stocks; if they lower it, the oversupply narrative will gain further traction.

Debate 2: The Battle of "Token Maximization" vs. "Token Minimization"

A new phenomenon has emerged in the deployment of AI applications: many enterprises initially encouraged employees to generate as many tokens as possible ("token maxing"), but this led to IT budget overruns. As a result, companies are now seeking cheaper alternatives.

Specifically:

- Enterprises are increasingly adopting open-source large language models (LLMs) to handle basic queries.

- Orchestration layers are being superimposed on top of frontier models to divert simple tasks to open-source models, reserving frontier models only for complex tasks.

- The market's focus is shifting to how token providers present this trend in their earnings reports and their guidance for the second half of 2026.

The conclusion is that while the second quarter of 2026 (June quarter) poses little issue for the AI supply chain, market anxiety has shifted toward the impact of cheaper tokens on second-half guidance.

Debate 3: Why Has Stock Re-rating Failed Post-LTA Signings?

The signing of Long-Term Agreements (LTAs) should have triggered a valuation rerating for memory stocks, yet the market response has been muted. The explanation points to vivid market memory—past LTAs were either renegotiated or ultimately forced customers to take on unwanted inventory (similar to the experience of analog semiconductor companies during COVID).

Of course, some argue that current memory LTAs hold structural (rather than cyclical) significance, provided AI demand remains robust. However, whether earnings estimates can continue to be revised upward remains the biggest uncertainty for investors—especially regarding when and by how much memory prices will continue to beat expectations, thereby driving 2028 EPS upward, as the timeline remains highly unclear.

Peaking Rate of Change: Three Dimensions Synchronized

The memory industry is nearing a "peak rate of change," manifested across three dimensions:

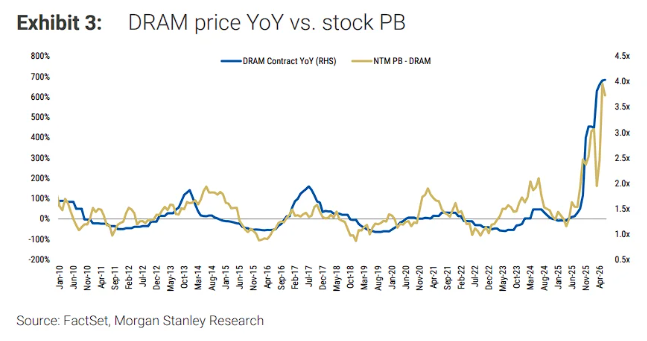

Year-on-Year Pricing (YoY pricing): DRAM price growth has slowed significantly from its Q1 highs, and subsequent quarterly gains are expected to continue narrowing.

Inventory Dynamics: The pace of improvement in the inventory cycle is leveling off.

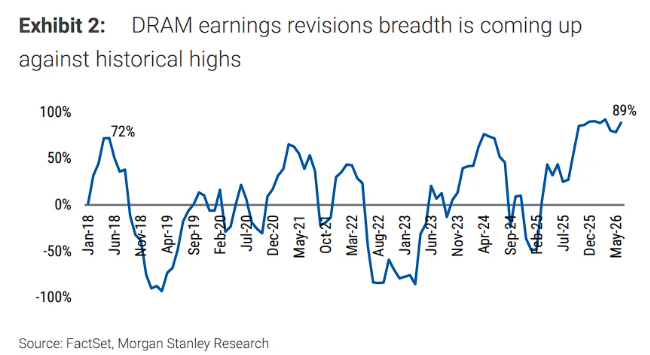

Breadth of EPS Revisions: The breadth of earnings revisions for the DRAM sector has hit historic highs (currently around 89%), leaving limited room for further upward revisions.

This "peak rate of change" signal is the core reason why memory stocks need a temporary breather.

Notably, since the rise of generative AI in November 2022, the memory sector has undergone three cyclical pullbacks. These pullbacks are characterized as normal corrections within a structural bull market, rather than the onset of a bear market.

At the same time, the most immediate pressure on the memory sector stems from positioning rather than a collapse in fundamentals.

Memory stocks represent one of the most crowded positions in the market. Recent increases in volatility have made maintaining historically high net exposure increasingly difficult. Over the past week, multiple investors expressed high sensitivity to this dynamic and showed strong interest in diversifying into laggard opportunities.

The recent weakness in hyperscaler stocks could be a leading indicator that memory stocks (as core beneficiaries of AI spending) are about to underperform the broader market. Seasonally, the current window is also a relatively challenging phase for the overall market.

Finally, at this stage of the cycle, the commentary from hyperscalers during earnings calls will influence stock prices far more than comments from memory companies' own management—as memory executives are highly likely to maintain an optimistic tone at this point in the cycle.

For AI spenders, the "token maximization" effect is expected to support Q2 2026 results, but whether Q3 2026 guidance falls short of market expectations will be the next major battleground. Potential downside risks include token usage optimization, competition from low-cost open-source LLMs, and the impact of "chipflation" on profit margins.