Research Digest | Explosive Returns Ahead? Wall Street’s Hottest 2 US Stocks for the AI & Data Boom

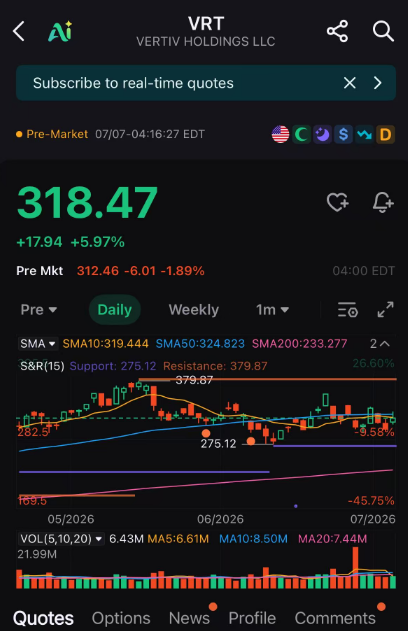

VERTIV HOLDINGS LLC VRT | 0.00 | |

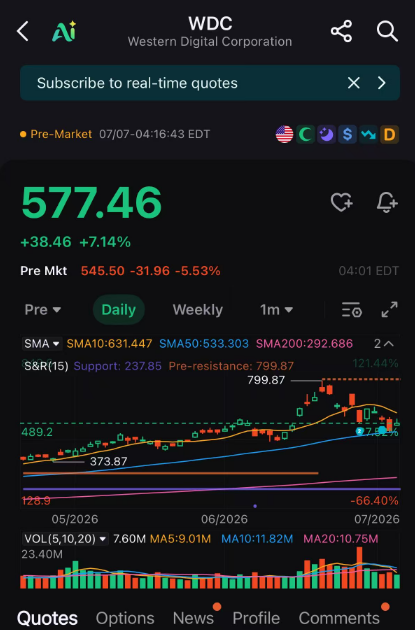

Western Digital Corporation WDC | 0.00 |

Subscribe to The Value Anchor Topic / The Trend Catcher Topic —unlock the full historical archive and never miss a weekly pick again.

Top 2 US Stocks with the Highest Potential Upside(31%, 81%)

| Stock | Key Catalyst (from data) | Top Wall Street View | Target Price |

|---|---|---|---|

| VERTIV HOLDINGS LLC(VRT.US) | AI power & cooling bottleneck; direct beneficiary of data center CapEx | Goldman Sachs (Buy): Listed as top AI infrastructure beneficiary | $416 (GS target) vs. $318 close |

| Western Digital Corporation(WDC.US) | HDD super cycle; severe supply-demand imbalance; pricing power | Melius Research (Buy): Street-high target; “golden pit” for re-entry | $1,050 (Melius PT) vs. $577 close |

1. VERTIV HOLDINGS LLC(VRT.US) – The AI Power & Cooling Bottleneck Enabler

- The Core Thesis: AI data centers are scaling at an unprecedented rate, but power and thermal management are the most constraining bottlenecks. Vertiv, as the market leader in critical digital infrastructure, is indispensable for every new AI data center build-out. Its revenue is directly tied to every new server rack deployed.

- Goldman Sachs' Explicit View: Buy. GS explicitly calls out Vertiv as a top AI infrastructure beneficiary. In their sector coverage, they highlight that AI high-power racks (like NVL72) require more complex power conversion and liquid cooling, directly benefiting Vertiv's product mix and ASP growth.

- Why VRT? It is the most direct “picks-and-shovels” play on the AI CapEx cycle that doesn't rely on memory or chip pricing volatility. With data center CapEx forecast to reach ~$725bn in 2026, a significant portion flows to power infrastructure. Its backlog gives 8+ quarters of revenue visibility, making it one of the most predictable growth stories in the AI ecosystem.

- Risk: Order lumpiness and execution on large-scale projects. A slowdown in hyperscaler CapEx would be the primary headwind.

2. Western Digital Corporation(WDC.US) – The HDD Super Cycle King

- The Core Thesis: The HDD market has entered a structural “super cycle” driven by an explosion in AI-generated data. Demand (driven by hyperscalers storing ~80% of data on HDDs) is growing 40-50% YoY, while supply is constrained to just 30-35% YoY. This creates a 10-15% supply gap that gives the HDD duopoly immense pricing power.

- Goldman Sachs' View: Buy. GS upgraded WDC into their “Conviction List - Buy,” citing the HDD cycle as a “once in a decade” opportunity. They explicitly point to the company's HDD incremental gross margins of 70-75% as a key driver for earnings upside.

- Why WDC? Unlike other storage plays, WDC benefits from a structural supply shortage, not just demand. The industry cannot easily add HDD capacity, meaning the pricing environment could remain strong into 2028. Its FCF margin is near 30%, making it less cyclical and more of a value-creating asset.

- Risk: If hyperscalers suddenly shift to all-flash storage, demand would be disrupted. Immediate risk is a disappointing earnings report on July 29.

Disclaimer: The content is provided as general information only and should not be taken as investment advice. All the contents shall not be taken as a recommendation to buy or sell any security or financial instruments. Any action you take resulting from information, analysis, or commentary on this article is your responsibility. Please consult your investment advisor before making any investments.