Research Digest | Meta’s Compute Sale Explained: Real Motives, Wall Street View, and What It Means for Your AI Stock Picks?

Meta Platforms META | 0.00 | |

CoreWeave CRWV | 0.00 | |

NVIDIA Corporation NVDA | 0.00 | |

Broadcom Limited AVGO | 0.00 | |

NEBIUS NBIS | 0.00 |

Subscribe to The Value Anchor Topic / The Trend Catcher Topic —unlock the full historical archive and never miss a weekly pick again.

Meta’s plan to lease excess computing power caused a sharp drop in AI hardware stocks amid concerns over capacity surplus and capital spending cuts. However, Wall Street banks say this isn’t a major industry shift—Meta’s capacity is limited, making the move a short-term EPS boost for Meta and a competitive test for companies like CoreWeave. The real impact will be clearer after earnings season.

Wall Street Views

| Company/Stock | Direct Impact | Bank View & Rating | EPS/Valuation Impact |

|---|---|---|---|

| Meta Platforms(META.US) | Renting compute, EPS buffer | UBS: Buy ($865); MS: Overweight ($775); Bernstein: Outperform ($850) | Short-term EPS boost, valuation led mainly by core AI products |

| CoreWeave(CRWV.US) | New competition | Bernstein: Underperform ($67) | Customer turns potential competitor; competition risk |

| NVIDIA Corporation(NVDA.US), Broadcom Limited(AVGO.US), NEBIUS(NBIS.US) | Stock sell-off | All: Watch for capex signals in Q2 earnings | Not pivot unless capex truly revised down |

Key Logic: Selling Compute Doesn’t Mean Global Surplus

Meta Platforms(META.US)’s cloud presence is relatively small compared to Amazon.com, Inc.(AMZN.US) and Alphabet Inc. Class A(GOOGL.US). Even if Meta leases out some capacity, it cannot alone shift the direction of global cloud construction. Bernstein points out that leaseable compute does not equal surplus compute; segment definitions differ.

Some investors assume that leasing compute = excess supply = capex cuts, but that’s oversimplified. Meta may occasionally lease out capacity, but that doesn’t mean the whole industry is facing oversupply. For example, Morgan

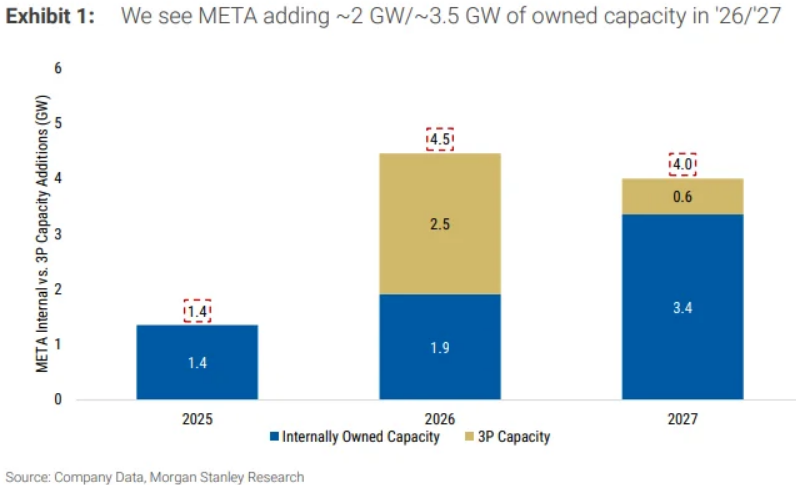

Stanley estimates Meta could add 2GW of new capacity in 2026 and 3.5GW in 2027, compared to Amazon and Google’s much larger additions. Even if Meta rents out a portion, it’s not enough to change the entire industry's build-out path.

Bernstein also notes Meta’s total capacity looks big, but it doesn’t all translate to “rentable AI compute”—nor is it all the same hardware, workload, or price. Notably, recent reports say Google has actually limited Meta’s compute access due to its own constraints, suggesting these moves are really about reallocating resources, not true surplus.

Meta's Record on "Selling Compute"

Meta’s handling of excess compute isn’t new. Mark Zuckerberg has previously discussed renting out unused capacity if internal needs fall short. Wall Street analysts consider this a practical bridge, not a new core business.

For Meta Shareholders: It's An EPS Bridge, Not A Business Pivot

UBS estimates renting compute could add up to 8% upside to Meta’s 2028 EPS for every 250MW leased for one year at ~$40/watt. Morgan Stanley sees it as a temporary buffer until new AI products scale up.

Capital Expenditure Not Necessarily Cut

Morgan Stanley currently projects Meta’s capex to rise significantly through 2028, emphasizing that renting compute doesn’t mean a change in the build-out for Meta’s core AI products. If Meta launches a full-scale cloud service, capex may actually increase.

Meta vs CoreWeave: Customer Turns Rival

Bernstein notes Meta is a key customer for CoreWeave(CRWV.US)—Meta contracts account for over a third of CoreWeave’s order backlog. If Meta rents compute, it could become a direct competitor, especially for renewals.

Why Did Hardware Stocks Fall?

Beyond fundamentals, the sell-off is exaggerated by crowded positions and profit-taking. The decline in CoreWeave (–13%) and Nebius (–15%) reflects concerns over business model shifts and potential new competition. Semiconductor holdings are at historic highs, so any “compute not rare” narrative triggers swift selling.

Wall Street Ratings & Key Risks

- UBS: Buy, target $865; sees rental as EPS bridge, not a new business.

- Morgan Stanley: Overweight, Top Pick, target $775; focus on advertising and main products.

- Bernstein: Outperform for Meta ($850), Underperform for CoreWeave ($67); rental increases Meta options, raises competitive risk for CoreWeave.

Risks: Ad cycles, regulations, uncertain Reality Labs returns, execution errors in data center build-outs.

Bottom Line:

Meta’s move to sell compute is a short-term EPS boost and a business model test for new cloud players. For investors, real signals will come with Q2/Q3 earnings and tech spending guidance. For now, don’t confuse “selling compute” with “AI hardware oversupply”—watch actual capex cycles and new product launches.

Disclaimer: The content is provided as general information only and should not be taken as investment advice. All the contents shall not be taken as a recommendation to buy or sell any security or financial instruments. Any action you take resulting from information, analysis, or commentary on this article is your responsibility. Please consult your investment advisor before making any investments.