Research Digest | The Meta - Anthropic Secret Talks: SemiAnalysis Sees Zuckerberg's Stealth Play Against Amazon and Google

Meta Platforms META | 0.00 | |

CoreWeave CRWV | 0.00 | |

NEBIUS NBIS | 0.00 | |

Amazon.com, Inc. AMZN | 0.00 | |

Alphabet Inc. Class A GOOGL | 0.00 |

The recent debate over Meta's expanding AI infrastructure has centered on one question: Is the company preparing to become a "neocloud" provider, and if so, what would that mean for the broader AI infrastructure market?

According to a new report from SemiAnalysis, investors may be drawing the wrong conclusion.

While headlines suggesting Meta Platforms(META.US) could rent out excess computing capacity triggered a selloff in AI infrastructure companies such as CoreWeave(CRWV.US) and NEBIUS(NBIS.US) amid renewed concerns about overcapacity, SemiAnalysis argues that Meta's aggressive investment in AI compute is more likely to accelerate than slow.

The research firm expects Meta's capital expenditures to remain elevated into 2027, supported by multiple potential monetization paths beyond training frontier AI models.

AI Infrastructure Buildout Continues to Accelerate

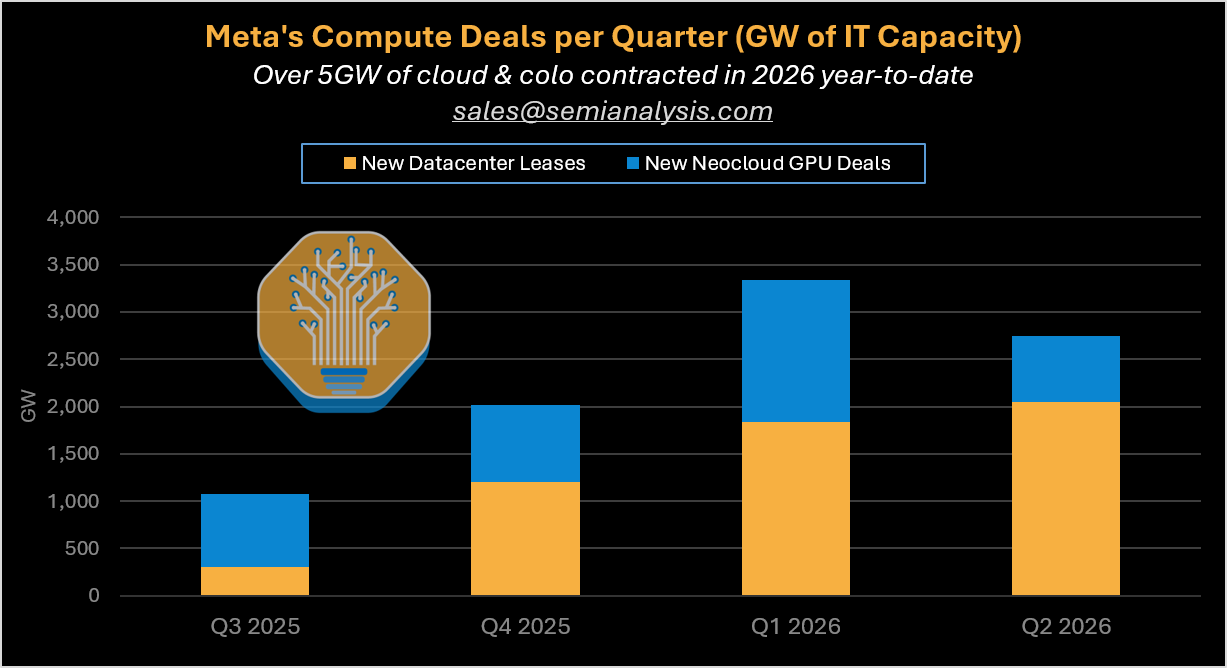

SemiAnalysis estimates that Meta has already contracted more than 5 gigawatts (GW) of compute capacity during the first half of 2026 through cloud providers and colocation partners, excluding its own self-built data centers.

The firm estimates Meta has signed nearly 10GW worth of compute-related agreements since early 2024, with third-party infrastructure now accounting for an increasing share of future capacity additions.

Rather than signaling weaker demand, the report argues that Meta's growing infrastructure footprint reflects increasing confidence that the company will find multiple high-value uses for its AI capacity.

Finding the strongest stocks inside the strongest sectors—so you can ride the market’s clearest trends.

Subscribe to The Trend Catcher Topic / The Value Anchor Topic —unlock the full historical archive and never miss a weekly pick again.

Four Potential Uses for Meta's Massive Compute Fleet

According to SemiAnalysis, Meta's expanding infrastructure could support four major initiatives simultaneously.

1. Training Frontier AI Models

The largest portion of new compute capacity is still expected to support Meta Superintelligence Labs (MSL), the company's flagship AI research effort.

SemiAnalysis believes Meta remains committed to competing with leading frontier model developers such as OpenAI and Anthropic, despite market speculation that it may scale back its ambitions.

2. Scaling Recommendation Systems

Beyond large language models, the report argues that Meta's recommendation algorithms could become an even larger consumer of AI infrastructure.

SemiAnalysis estimates Meta could increase the computational complexity of its advertising recommendation systems by more than 10x, requiring significantly more training and inference capacity.

More sophisticated recommendation models could improve advertising efficiency while supporting higher pricing and stronger monetization across Meta's platforms.

3. Building an AI Platform Similar to Amazon Bedrock

One of the report's more notable predictions is that Meta could evolve into an AI platform provider.

SemiAnalysis claims Meta is in late-stage discussions with Anthropic regarding access to private Claude model deployments, although neither company has publicly confirmed such negotiations.

If realized, Meta Platforms(META.US) could eventually offer enterprise AI services similar to Amazon.com, Inc.(AMZN.US) Bedrock or Alphabet Inc. Class A(GOOGL.US) Vertex AI, allowing customers to access foundation models through Meta's own infrastructure.

Initially, such capabilities may primarily serve Meta's internal needs before expanding to enterprise customers.

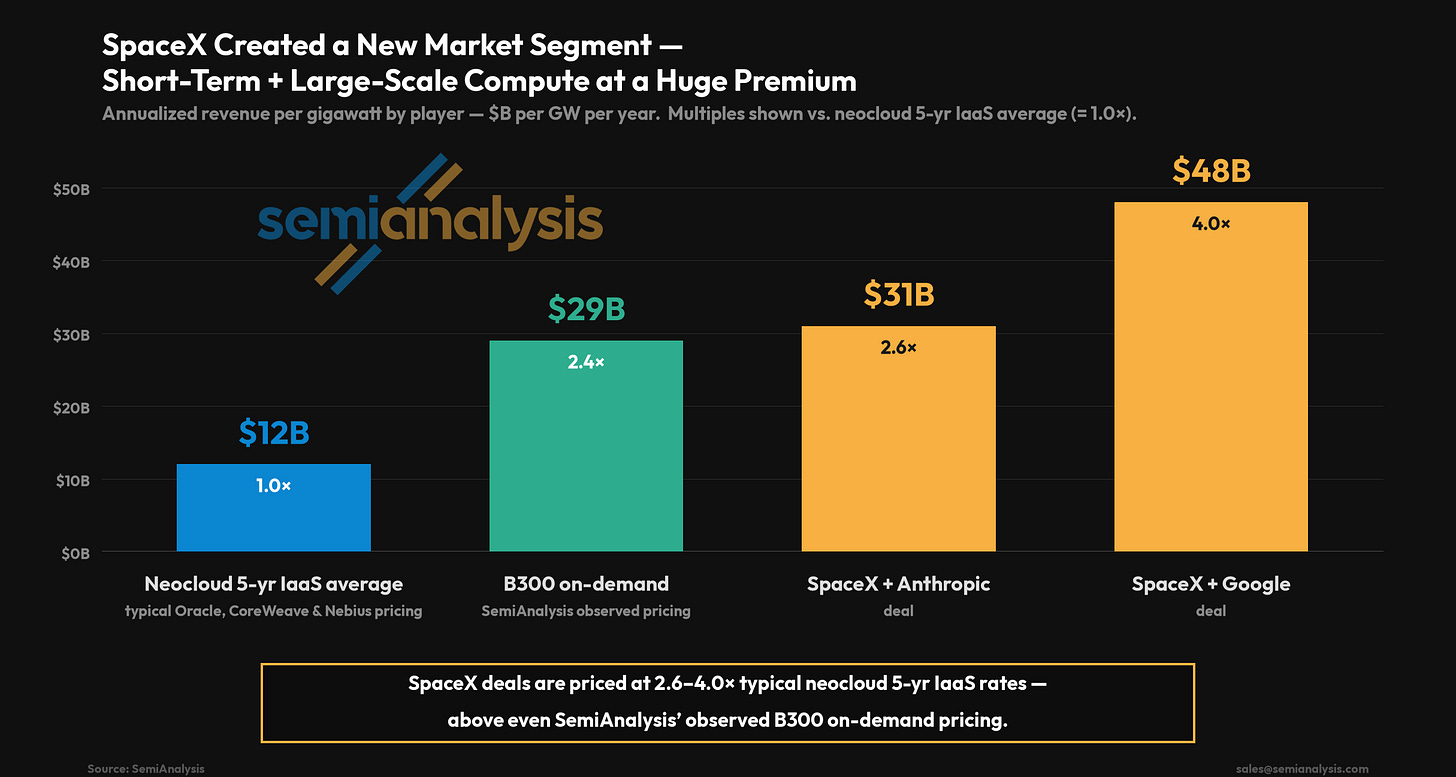

4. Selling High-End AI Compute

The report also argues Meta could selectively commercialize portions of its AI infrastructure by renting premium computing capacity to external customers.

SemiAnalysis compares this opportunity to recent high-profile compute agreements involving SpaceX(SPCX.US), which reportedly secured premium pricing for large-scale AI infrastructure contracts.

The research firm estimates that allocating just a few hundred megawatts of compute to external customers could potentially generate more than $10 billion in annual revenue, although this represents a theoretical scenario rather than company guidance.

Why More Compute Doesn't Necessarily Mean Oversupply

Instead of viewing Meta's growing capacity as a sign of future oversupply, SemiAnalysis argues investors should see it as creating strategic flexibility.

If Meta's frontier AI ambitions continue progressing, additional infrastructure would support model development.

If demand shifts elsewhere, the company could instead deploy capacity toward recommendation systems, enterprise AI services, or commercial compute offerings.

This optionality, according to the report, makes continued investment in AI infrastructure economically attractive even if one business line underperforms expectations.

Potential Beneficiaries Could Include AI Infrastructure Providers

The report also suggests Meta is likely to remain a major customer for external infrastructure providers despite its own aggressive buildout.

Because much of Meta's future capacity is expected to come from leased facilities and cloud partners, companies such as CoreWeave(CRWV.US) and NEBIUS(NBIS.US) could continue benefiting from Meta Platforms(META.US)'s expanding AI investment cycle.

Rather than replacing third-party providers, SemiAnalysis expects Meta's compute demand to remain large enough to support continued outsourcing alongside internal data center expansion.

SemiAnalysis concludes that Meta's AI infrastructure strategy should not be viewed solely through the lens of building larger AI models.

Instead, the firm believes the company's rapidly expanding compute footprint represents a broader platform strategy with multiple potential revenue streams—from advertising optimization and enterprise AI services to premium infrastructure offerings.

If that thesis proves correct, Meta's AI spending may remain one of the largest drivers of demand across the AI infrastructure ecosystem for years to come.