Rivian Automotive (RIVN) Valuation After Uber R2 Order And Adjusted Capital Plan

Rivian Automotive RIVN | 0.00 |

Rivian Automotive (RIVN) is back in focus after securing an order from Uber for up to 50,000 R2 SUVs, as well as reshaping its capital plan through a fresh loan agreement and new funding tools.

The recent Uber order and capital reshaping are landing against a weak recent trend, with the stock down 19.97% on a 30 day share price return and 28.95% year to date, while the 3 year total shareholder return of 2.38% suggests only modest long run progress so far.

If you are watching how EV and autonomy stories play out beyond Rivian, this is a good moment to size up other opportunities through 64 profitable AI stocks that aren't just burning cash

With the stock down sharply this year, yet trading at an intrinsic value discount of about 52% and around 32% below the average analyst price target, the key question is whether Rivian is mispriced or if the market already reflects its future growth.

Most Popular Narrative: 45.7% Undervalued

According to the most followed narrative on Rivian, the fair value sits at $25.41 versus the last close at $13.79, which puts a big gap between narrative expectations and the current share price.

Gen2 R1T and R1S, refinement from feedback and lower cost building.

R2, R3 and R3X lower cost options for different audience.

JV with VW and the ripple effects for Software and Electrical Architecture deals through not just VW but also others. Utilizing Supplier leverage from VW.

Amazon expanding EDV's in Europe with recent order. Europe expansion in general.

RJ's focus on what's important approach while keeping out of politics and remaining neutral gives others including that are building up hate for Tesla a great alternative.

Revenue from existing and expanding charging infrastructure, not just for Rivian's but also third party OEM's.

Gross Profitability guidance for FY25.

The fair value hinges on a broad product lineup, a major auto partner, and new revenue streams. The tension is whether those pieces scale fast enough.

Result: Fair Value of $25.41 (UNDERVALUED)

However, this depends on Rivian turning its annual net loss of US$3,517.0m and its capital heavy expansion into sustainable profitability without straining its balance sheet.

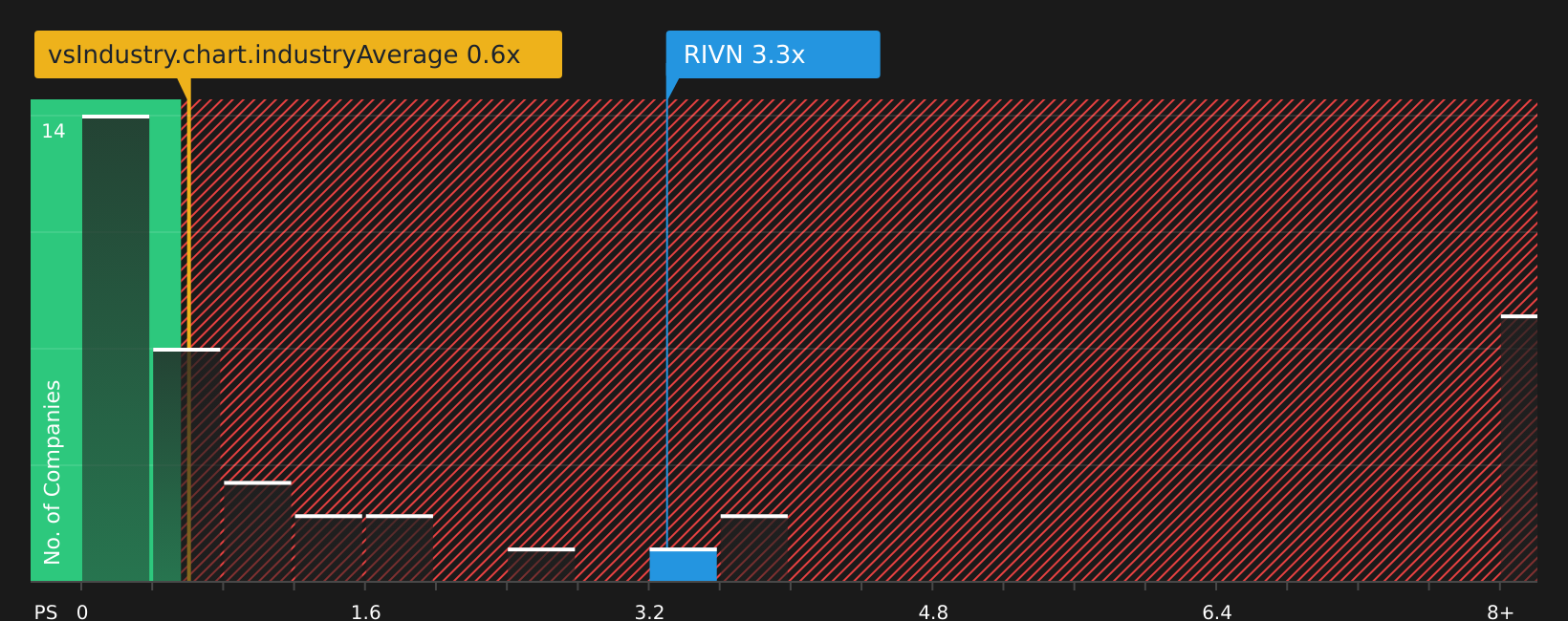

Another View: Pricing Looks Stretched On Sales

While the user narrative and DCF estimate suggest Rivian is undervalued at $13.79, the market is paying a P/S of 3.2x. That is rich compared with the US Auto industry at 0.6x, peers at 1x, and a fair ratio of 1.7x, which points to meaningful valuation risk if sentiment cools.

For readers who lean more on relative pricing than cash flow models, this gap between current P/S, peers, and the fair ratio raises a simple question: is the stock priced for a smoother journey than its fundamentals currently show, or is the market underestimating future progress, See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With sentiment clearly split between risk and upside, this is a good time to review the full picture yourself and decide how you feel about Rivian's path, including 2 key rewards and 1 important warning sign

Looking for more investment ideas?

If you stop at one stock, you miss the bigger picture, so use the screener to quickly spot other ideas that fit the way you like to invest.

- Target potential bargains that combine quality and price by scanning 51 high quality undervalued stocks that currently line up with your preferred yardsticks.

- Focus on resilience first and returns second with a curated list of 65 resilient stocks with low risk scores tailored to calmer portfolios.

- Explore a focused screener containing 21 high quality undiscovered gems to review companies based on their fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.