Rivian (RIVN) Stock Looks Expensive As Delivery Outlook Rises

Rivian Automotive RIVN | 0.00 |

Rivian Automotive stock has climbed about 36.0% over the past year, yet its broader valuation checks lean expensive, so the recent gains sit against a reading that the shares are not a clear bargain.

- Over the past year, Rivian's 36.0% share price gain puts the stock firmly in recovery territory. This can raise the bar for what counts as good value from here.

- Fresh capital raised through a large share offering may support Rivian's production and factory plans. At the same time, ongoing cash burn and shareholder dilution concerns can weigh on what investors are willing to pay for that growth.

- With a low value score of 2 out of 6 checks, Rivian currently screens as leaning expensive rather than a clear bargain on the broader valuation tests.

For investors, the debate is whether Rivian's recent share price recovery already reflects its growth ambitions or still leaves room for a more attractive entry on valuation grounds.

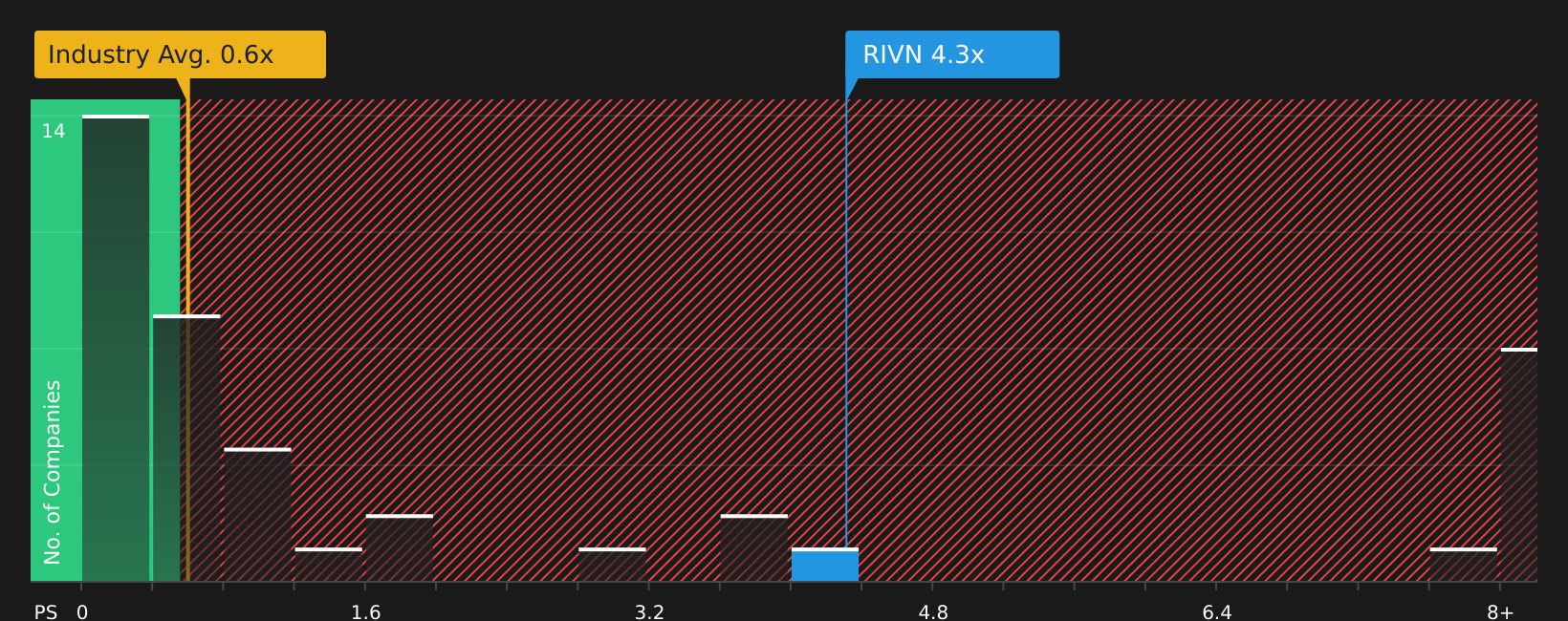

Is Rivian Automotive Getting Expensive on Sales?

The P/S multiple is often a clean way to compare a high-investment-phase business like Rivian Automotive when earnings are still negative.

Rivian currently trades on a P/S ratio of about 4.5x, compared with an auto industry average of around 0.6x and a peer average near 0.7x. On a tailored basis, the fair P/S that takes into account Rivian's size, risks and sector is closer to 1.9x, so the current multiple is more than double what that framework suggests. Despite recent share issuance to fund growth plans and the market reaction to dilution concerns, the stock price still reflects a much richer sales multiple than both the industry and the fair ratio imply.

For investors, that means the market is already assigning a premium price to each dollar of Rivian revenue relative to typical auto stocks and to what the model indicates as a more balanced level.

On this P/S measure, Rivian Automotive stock currently appears overvalued.

The Rivian Automotive Narrative: What Would Justify Today's Price?

Simply Wall St Narratives pick up where Rivian Automotive's valuation puzzle leaves off by spelling out which future paths for growth, margins and earnings would need to play out for the stock to be priced meaningfully higher or lower than it is today. These Narratives are available on Simply Wall St's Community page. Each Narrative sets out a fair value as a thesis about Rivian Automotive's business that can be revisited over time, rather than a one off snapshot.

Community views on Rivian Automotive sit far apart, with one camp seeing long term upside potential and another focused on execution and policy risks.

Bull case: roughly fairly valued

"Vertical integration in technology, especially in autonomy, battery, and software, combined with growing software & services revenue (including licensing via partnerships like with Volkswagen) is expected to open new high-margin revenue streams and diversify earnings, potentially strengthening EBITDA and net margins over time…"

Bear case: 88% overvalued

"Shrinking policy support, cost inflation, and low demand threaten Rivian's margins, cash flow, and ability to justify ambitious expansion plans…"

Do you think there's more to the story for Rivian Automotive? Head over to our Community to see what others are saying!

The Bottom Line

For Rivian Automotive, the core issue is that the stock is already priced at a premium on sales compared with both the wider auto industry and a tailored fair multiple. That leaves less room for error if the growth story, cost discipline or funding path disappoint from here. The crux of the bull versus bear debate is whether Rivian can eventually translate its investment and partnerships into enough scalable, higher margin revenue to make today's rich P/S multiple feel reasonable rather than stretched.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.