RTX (RTX) Stock Near Fair Value After $100 Million Defense Expansion

RAYTHEON TECHNOLOGIES CORPORATION RTX | 0.00 |

RTX (RTX) is back in focus after Raytheon committed US$100 million to expand its Portsmouth, Rhode Island facility, a move tied to higher demand for LTAMDS radar and Patriot GEM-T components.

The Rhode Island expansion comes as RTX’s share price has pulled back 3.62% over the past day to US$185.60, yet still shows a 6.37% 30 day share price return and a 5 year total shareholder return of 138.56%, suggesting longer term momentum remains intact.

If RTX’s defense exposure has your attention, it could be a good moment to look across the sector and see which other contractors are moving through the 34 power grid technology and infrastructure stocks

With RTX trading at US$185.60, sitting roughly 16% below the average analyst price target and close to narrative fair value estimates, the key question is whether this reflects a genuine discount or a stock for which the market is already pricing in future growth.

Preferred P/E of 34.4x: Is It Justified?

With RTX stock at $185.60 and carrying a P/E of 34.4x, the market is assigning a relatively full earnings multiple, yet comparative data suggests investors are not paying a premium versus similar aerospace and defense companies.

The P/E ratio compares the current share price to earnings per share and is a common way to see how much investors are willing to pay for each dollar of profit. For a company like RTX, with a large installed base across Collins Aerospace, Pratt & Whitney and Raytheon, P/E is often used as a shorthand for what the market thinks about the durability and growth of its earnings.

According to the provided checks, RTX is considered good value based on its P/E of 34.4x versus an estimated fair P/E of 35.5x. It is also assessed as trading at good value compared with both the US Aerospace & Defense industry average P/E of 40.3x and a peer average P/E of 55.8x. That points to a situation where the market is paying up for RTX's earnings, but still at a lower multiple than many direct peers. Some investors may pay attention to this if valuations across the sector converge over time.

Looking at it another way, RTX is flagged as trading at good value relative to peers and industry overall, even though its forecast earnings growth of 9.89% per year is not classified as high and is expected to be slower than broader US market earnings growth. If sector valuations remain clustered around higher P/E levels, the fair P/E estimate of 35.5x gives a reference point that some investors may use as a potential level for where the market could gravitate, depending on how RTX's earnings and balance sheet evolve.

Result: Price-to-Earnings of 34.4x (ABOUT RIGHT)

However, RTX stock still faces risks, including potential program delays or defense budget changes that could challenge current earnings assumptions and reduce support for the price-to-earnings ratio.

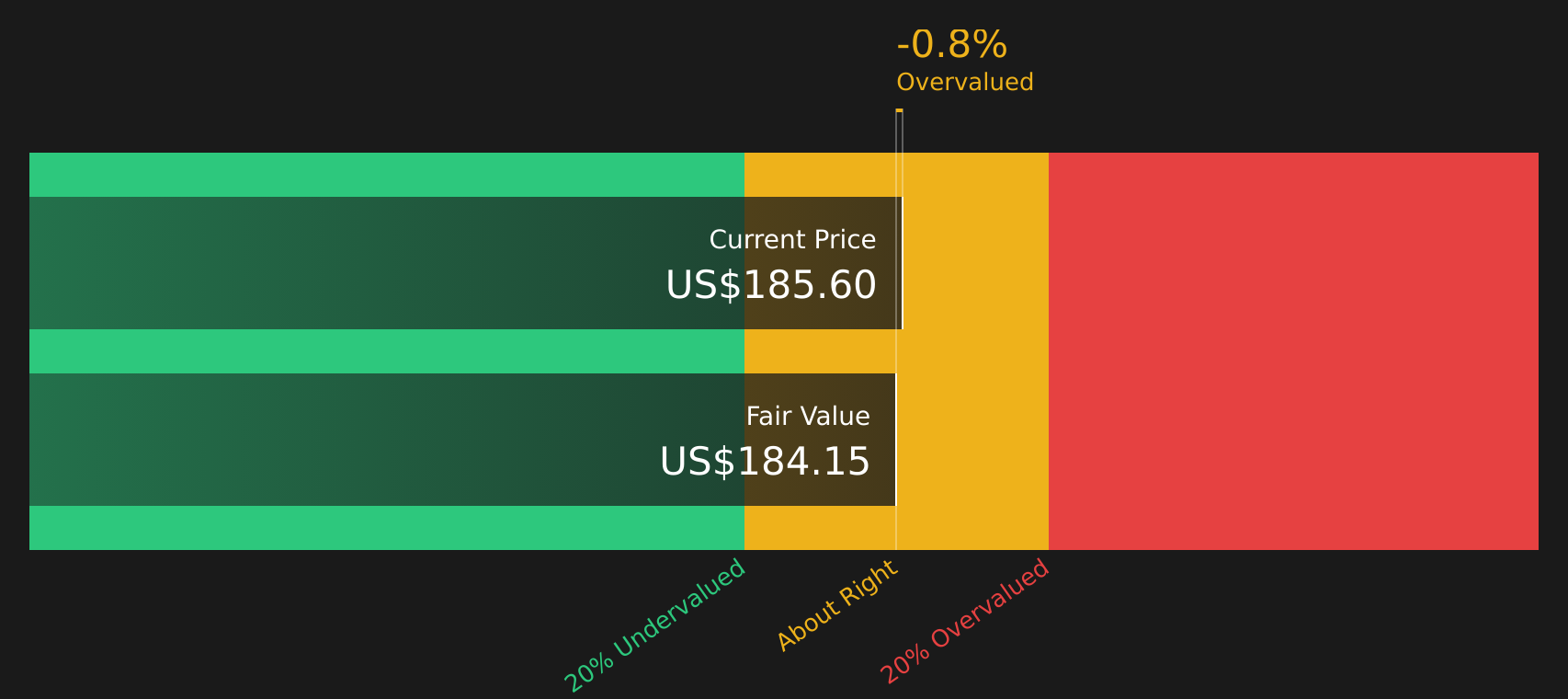

Another View on RTX: DCF Says the Market Is Already There

The P/E work suggests RTX stock is roughly in line with a fair ratio, but the SWS DCF model paints an even tighter picture. At $185.60, RTX is essentially level with an estimated future cash flow value of $185.50, leaving little obvious upside or downside from this lens.

When one method points to some relative value and another suggests the price already matches future cash flows, which signal should carry more weight for you as an investor?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out RTX for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 45 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Given the mixed signals around RTX, does the risk reward trade off feel balanced enough for you, or tilted one way? To pressure test your own view against both the concerns and the potential upside flagged by the market, it is worth reviewing the 4 key rewards and 2 important warning signs.

Looking For More Investment Ideas Beyond RTX?

If RTX has sharpened your interest in defense and industrials, consider broadening your watchlist with other opportunities that could suit your goals and risk comfort.

- Target potential mispricings by scanning companies that appear overlooked on valuation through the 45 high quality undervalued stocks.

- Strengthen your focus on capital preservation by reviewing companies screened as 65 resilient stocks with low risk scores.

- Hunt for quality stories flying under the radar with the screener containing 20 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.