Salesforce, Inc. (NYSE:CRM) May Have Run Too Fast Too Soon With Recent 28% Price Plummet

Salesforce.com, inc. CRM | 171.31 171.50 | -0.87% +0.11% Post |

Salesforce, Inc. (NYSE:CRM) shareholders won't be pleased to see that the share price has had a very rough month, dropping 28% and undoing the prior period's positive performance. The drop over the last 30 days has capped off a tough year for shareholders, with the share price down 43% in that time.

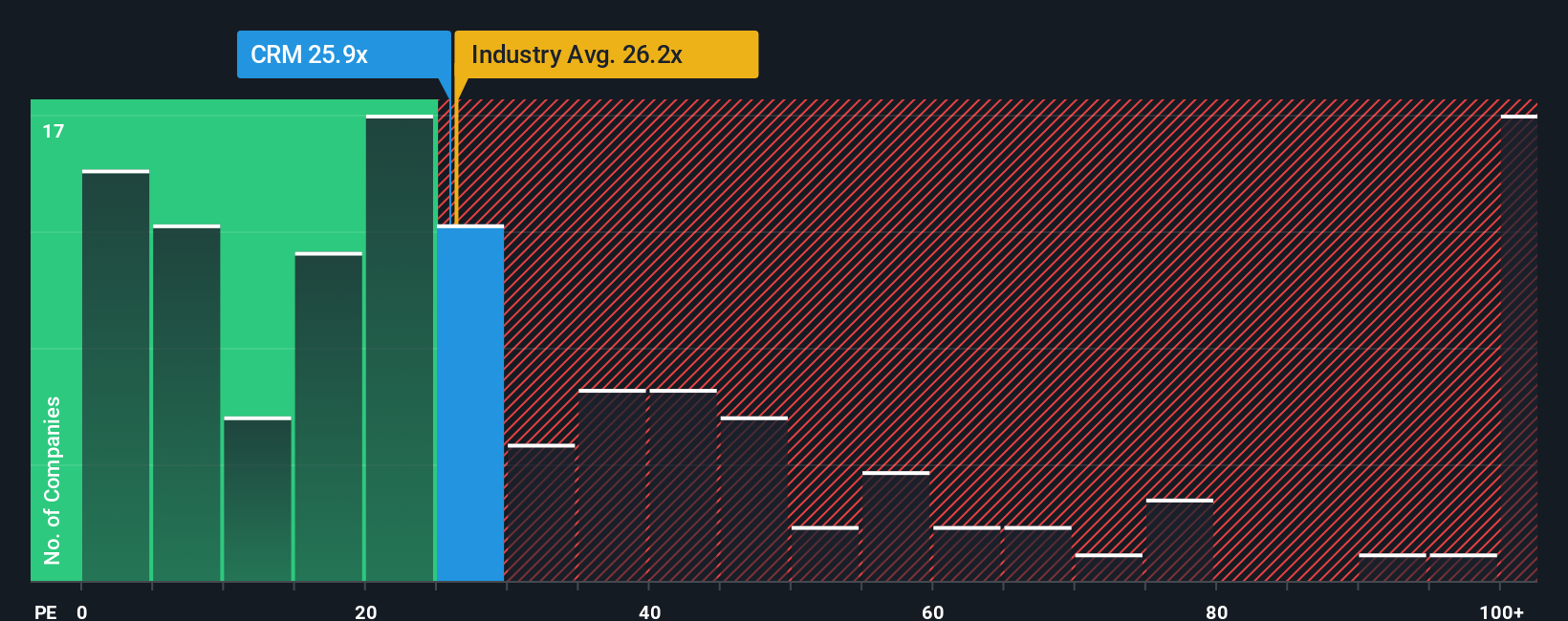

Even after such a large drop in price, given around half the companies in the United States have price-to-earnings ratios (or "P/E's") below 19x, you may still consider Salesforce as a stock to potentially avoid with its 24.6x P/E ratio. However, the P/E might be high for a reason and it requires further investigation to determine if it's justified.

Salesforce certainly has been doing a good job lately as it's been growing earnings more than most other companies. The P/E is probably high because investors think this strong earnings performance will continue. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

What Are Growth Metrics Telling Us About The High P/E?

The only time you'd be truly comfortable seeing a P/E as high as Salesforce's is when the company's growth is on track to outshine the market.

Retrospectively, the last year delivered an exceptional 23% gain to the company's bottom line. The latest three year period has also seen an excellent 2,652% overall rise in EPS, aided by its short-term performance. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

Looking ahead now, EPS is anticipated to climb by 13% per year during the coming three years according to the analysts following the company. Meanwhile, the rest of the market is forecast to expand by 12% per year, which is not materially different.

With this information, we find it interesting that Salesforce is trading at a high P/E compared to the market. It seems most investors are ignoring the fairly average growth expectations and are willing to pay up for exposure to the stock. Although, additional gains will be difficult to achieve as this level of earnings growth is likely to weigh down the share price eventually.

What We Can Learn From Salesforce's P/E?

There's still some solid strength behind Salesforce's P/E, if not its share price lately. Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

We've established that Salesforce currently trades on a higher than expected P/E since its forecast growth is only in line with the wider market. Right now we are uncomfortable with the relatively high share price as the predicted future earnings aren't likely to support such positive sentiment for long. Unless these conditions improve, it's challenging to accept these prices as being reasonable.

A lot of potential risks can sit within a company's balance sheet. You can assess many of the main risks through our free balance sheet analysis for Salesforce with six simple checks.

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with a strong growth track record, trading on a low P/E.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.