SentinelOne (S) Gains Attention Following Cyber Threat Warning, Is It Getting Expensive?

SentinelOne, Inc. Class A S | 0.00 |

A joint advisory from U.S. and international security agencies warning of Russian state-sponsored cyber threats to critical infrastructure has pushed cybersecurity stocks, including SentinelOne (S), into sharper focus for investors.

Beyond the immediate reaction to the cyber advisory, SentinelOne’s share price has shown building momentum, with a 30 day share price return of 28.90% and a year to date share price return of 33.74%, although the 5 year total shareholder return of 58.43% remains weak.

If the renewed focus on cybersecurity has your attention, this could be a good moment to scan the wider opportunity set with our screener of 31 AI small caps.

After SentinelOne’s sharp recent gains, the stock now sits at a very different entry point. The real issue is whether the current valuation still leaves enough upside potential to justify the risks.

Most Popular Narrative: 2% Overvalued

SentinelOne last closed at $19.58, slightly above the most followed narrative fair value of about $19.15. This frames the current move after the cyber advisory as only a modest premium to that assessment.

Expansion beyond endpoint security into high-demand adjacent markets such as cloud security, identity, and data protection, including the Prompt Security acquisition for GenAI risk, unlocks significant cross-sell opportunities and is expected to elevate average contract value and diversify revenue streams, laying the groundwork for outsized multi-year revenue growth.

Curious what justifies paying close to $20 a share for an unprofitable cybersecurity stock? This narrative leans on brisk revenue expansion, a sharp margin shift, and a premium future earnings multiple usually reserved for sector leaders.

Result: Fair Value of $19.15 (OVERVALUED)

However, SentinelOne’s reliance on large partners, along with the risk that acquisitions pressure margins before contributing meaningfully to revenue, could both undermine this upbeat narrative.

Another View on SentinelOne’s Valuation

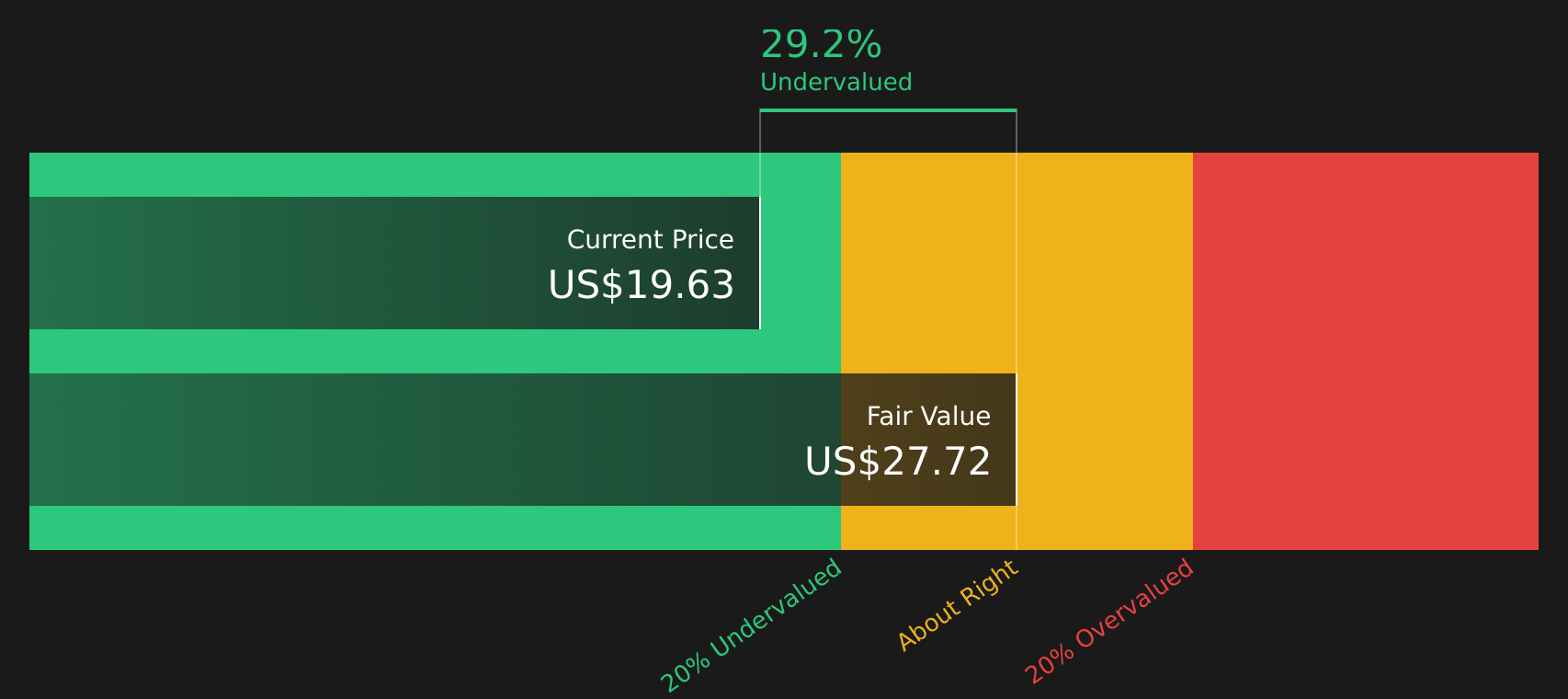

While the popular narrative pegs SentinelOne as about 2% overvalued around $19.15, the SWS DCF model points the other way, suggesting a fair value closer to $27.73, or roughly 29% above the current $19.58 price. Which set of assumptions do you find more realistic?

For a closer look at how that cash flow based estimate is built, including the key levers you might agree or disagree with, Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out SentinelOne for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 47 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals on SentinelOne’s valuation and narrative, are you ready to pressure test the story yourself and move fast on your own judgment? To weigh both sides in one place, review the 2 key rewards and 2 important warning signs

Looking for more investment ideas beyond SentinelOne?

If SentinelOne has you thinking more broadly about opportunities, do not stop here. Widen your search now or you risk missing stocks that better fit your goals.

- Target quality at a discount by reviewing our list of 47 high quality undervalued stocks that combine attractive pricing with stronger fundamentals.

- Strengthen your income stream by checking out 10 dividend fortresses that may suit investors who prioritise regular cash returns.

- Reduce portfolio stress by focusing on 78 resilient stocks with low risk scores designed for investors who want steadier business profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.