Sequence Risk: Why First Five Years Of Retirement Matter Most

Two retirees begin retirement with identical portfolios. They withdraw the same percentage of their savings each year. They experience the same average market returns over decades. Yet one runs out of money early, while the other maintains a comfortable income through retirement. The difference between their outcomes comes down to when market gains and losses occur.

This is the essence of sequence of returns risk — the idea that the order of investment returns matters, not just the average return itself. When retirees withdraw money during a downturn, they lock in losses.

Early negative years can shrink a portfolio in a way that later market gains may not fully undo — especially in the first years after retirement, when portfolios are largest, and withdrawals begin. Financial research across multiple institutions highlights the importance of this timing effect for retirement outcomes.

What Is Sequence Risk?

Sequence risk refers to the threat that market losses early in retirement can reduce a portfolio much more quickly than losses that occur later. In a situation where money is only contributed and not withdrawn, the sequence of returns doesn't really matter.

Over many years, gains and losses average out. However, in retirement, when regular withdrawals are made, the order becomes critical.

When markets fall early in retirement, and you still need to take money out, fewer assets remain to benefit from future rebounds. If the same drop occurs later, when fewer withdrawals are required, and the portfolio is smaller, the impact on long-term income tends to be less severe.

Research tied this risk to withdrawal strategies decades ago, including early work by William Bengen, whose safe withdrawal rate studies implicitly account for this timing effect.

Why the First Five Years Matter Most

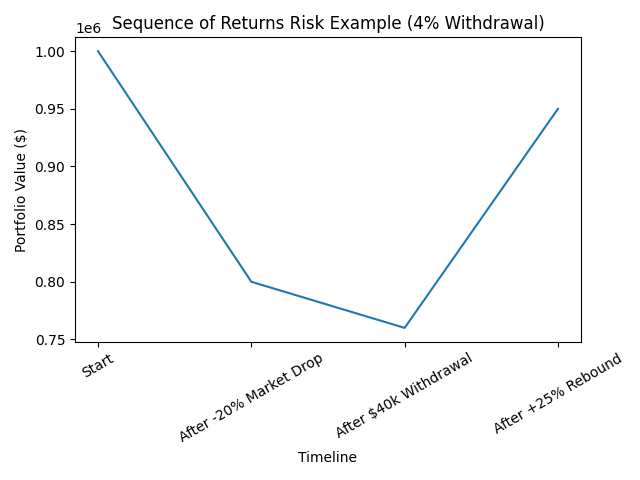

A simple example makes the concept practical. Imagine a retiree with a $1 million portfolio who follows a 4% withdrawal rate, meaning $40,000 a year for living expenses.

If the market falls 20% in the first year:

The portfolio drops to $800,000.

After a $40,000 withdrawal, it sits at $760,000.

If markets increase 25% the following year, the value of that $760,000 will be $950,000, which is less than the initial value of 1 million. Since the portfolio was low at the time of the withdrawals, the number of shares/assets to be involved in the recovery process is lower.

The early combination of losses and withdrawals can have a lasting effect that is hard to overcome by later positive performance. That is why financial planners and research reports single out the initial years of retirement as a period when sequence risk is most potent.

What Increases Sequence Risk

Certain conditions make a retiree more vulnerable to sequence risk:

- High equity allocations at retirement — Stocks can offer growth but also volatility. A large stock exposure at the moment of withdrawal increases downside exposure early on.

- High initial withdrawal rates — Withdrawing more out of a portfolio during decreasing values causes future returns to reduce more quickly.

- A bear market at retirement – Commencing retirement just as the markets fall implies that the losses will occur during times of retirement, and therefore will not be able to withstand the volatility.

- Rigid spending plans – A strategy that is not flexible to market forces can decimate the resources more quickly in adverse market climates.

- No cash buffer – It means that unless there are highly liquid funds available to meet immediate short-term requirements, retirees will be forced to sell investments at a loss instead of taking from reserves.

These factors influence how much the sequence of returns affects a particular retirement plan, independent of the long-term average of the portfolio.

Strategies Retirees Use to Manage Sequence Risk

A variety of strategies are usually employed by financial planners to reduce sequence risk without sacrificing long-term growth:

- Cash reserves to meet short-term requirements – Reserving 1-3 years of expenditure in cash or equivalents helps avoid the forced disposal of investments when times are tough.

- Bond ladders — Staggered bond maturities generate scheduled income, which can pay off near term withdrawals, and longer portfolios work towards long term growth.

- Dynamic withdrawal strategies — This means withdrawing according to the performance of the portfolio, including spending less during a down market, to help preserve money.

- Guardrail methods like Guyton-Klinger rules — These dictate rules that put spending on the path of adjustment under the event that a portfolio is below or above a prescribed level.

- Delaying Social Security — This means spreading out the Social Security benefit to much later in life, thus increasing the benefits of the investments made at the beginning of retirement.

- Part-time income in early retirement — Supplementary income can be used to offset expenses by reducing the need to access investment assets when markets are weak.

These plans are backed by research of firms, such as Vanguard and Fidelity Investments, which consider the sequence risk in their retirement planning advice.

Does Sequence Risk Mean Retirees Should Avoid Stocks?

Sequence risk does not imply retirees should eliminate stock exposure. Stocks remain a major source of long-term growth that is required to support income over 25-30 years of retirement. Full withdrawal from stocks makes longevity risk higher – the risk resulting in a portfolio failure due to its slow growth being insufficient to finance decades of expenditure.

The issue is structure, not avoidance of risk. A combination of growth, income, and liquidity assets in the portfolio may offer a balance between potential returns and volatility control. Aggressive allocation can aggravate sequence risk, and insufficient allocation can trail inflation and inhibit growth potential.

This underlines the fact that volatility and inflation should be managed at the same time. This trade-off is identified in decision frameworks that combine stocks with bonds and cash and vary spending in response to market conditions.

What Investors Should Consider Before Retiring

Practical questions to consider include:

- What withdrawal rate will you apply? Lower rates reduce pressure on the portfolio during downturns.

- Do you have 2–3 years of spending outside equities? This reduces the likelihood of selling assets at depressed prices.

- How flexible is your planned spending? Will you adjust if markets perform poorly early on?

- When do you plan to claim Social Security? Later claims may reduce early withdrawal needs.

- How diversified is your portfolio across asset types, sectors, and regions?

Reflecting on these questions before you retire could help you understand the extent to which sequence risk affects your retirement plans and which tools can help you address it effectively.

Bottom Line

Sequence risk is the timing of returns on investments and how premature losses, coupled with withdrawals, can shorten the lifespan of a retirement portfolio. The first five years of retirement are the most important, since this is when withdrawals are made, portfolios are at their largest, and market timing effects are most important.

Liquidity incorporation, spending adjustments during market downturns, and portfolio design to balance growth and stability can help retirees mitigate this risk without sacrificing the possibility of long-term income.

Benzinga Disclaimer: This article is from an unpaid external contributor. It does not represent Benzinga’s reporting and has not been edited for content or accuracy.