SFL (SFL) Orders LNG Car Carrier, Is The Stock Still 10% Undervalued?

SFL Corporation Limited SFL | 0.00 |

SFL (SFL) has ordered a 7,000-CEU LNG dual-fuel Pure Car and Truck Carrier for delivery in 2029, aligning its fleet with tighter environmental requirements and increasing demand for global car shipment capacity.

Alongside the new LNG dual-fuel carrier order, SFL has been added to several Russell growth benchmarks. The stock’s share price return has moved 34.22% year to date, with a 5 year total shareholder return of 123.64%, suggesting momentum has been building over the longer term despite some recent pullback.

If this kind of fleet transition has you thinking about broader themes, it could be a good moment to look at other transport and infrastructure ideas through the 35 power grid technology and infrastructure stocks

With SFL shares up 34.22% year to date and trading at a modest 7.7% discount to one intrinsic value estimate and 10.7% below an analyst price target, you have to ask: is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 9.7% Undervalued

Compared with the last close at $10.59, the most followed narrative for SFL points to a fair value of $11.73, creating a modest valuation gap that hinges on how its fleet renewal and contracted cash flows play out.

SFL's ongoing investment in modern, fuel-efficient, and LNG-capable vessels along with substantial efficiency upgrades positions the company to benefit from tightening environmental regulations and growing demand for lower-emission shipping, supporting higher utilization rates, improved charter terms, and strengthening net margins and long-term earnings stability.

Curious what earnings path and margin profile need to line up for that price target to work. The narrative leans heavily on recurring charter income, higher profitability, and a richer future earnings multiple to bridge the gap between today’s price and that $11.73 fair value.

Result: Fair Value of $11.73 (UNDERVALUED)

However, SFL's heavy exposure to oil related assets and large capital commitments for new vessels could pressure cash flow and weaken the long term dividend and buyback story.

Another View on SFL’s Valuation

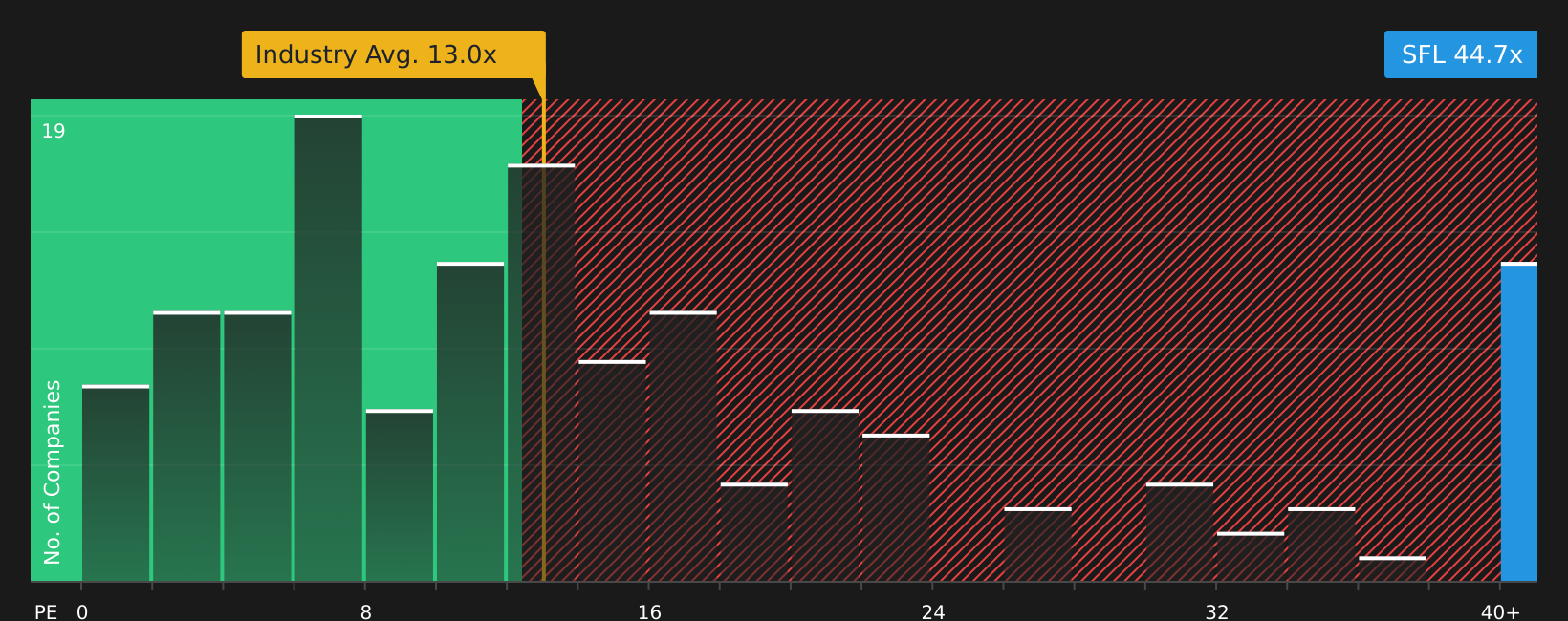

The first narrative leans on discounted cash flows and points to SFL trading around 7.7% below one fair value estimate. On earnings, though, the picture shifts, with SFL on a P/E of 44.7x versus a peer average of 13.2x and a fair ratio estimate of 33.4x. This suggests investors are paying a much richer price for each dollar of current earnings and taking on valuation risk if forecast growth or margins slip.

This gap between cash flow based value support and a high earnings multiple raises an obvious question for anyone looking at SFL today: which of these signals carries more weight in your own process, the modelled cash flows or what the market is already paying for near term earnings?

Next Steps

Mixed messages on SFL so far? If you care about both what could go right and what could go wrong, take a moment to weigh the 2 key rewards and 3 important warning signs.

Looking for more investment ideas beyond SFL?

If SFL has sharpened your focus on where to put fresh capital, do not stop here. Broaden your watchlist with a few targeted idea lists.

- Spot potential mispricings early by scanning companies that screen as high quality yet overlooked via the screener containing 18 high quality undiscovered gems.

- Strengthen your core holdings by reviewing the solid balance sheet and fundamentals stocks screener (47 results) to see which stocks pair cleaner balance sheets with resilient fundamentals.

- Prioritize resilience by checking the 74 resilient stocks with low risk scores so you are not the one hearing about lower risk opportunities after the move has already happened.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.