Stanley Black And Decker (SWK) Stock Could Be 28.87% Undervalued After Margin Progress

Stanley Black & Decker, Inc. SWK | 0.00 |

Engineered Fastening and DEWALT momentum reshape the Stanley Black & Decker stock story

Stanley Black & Decker (SWK) stock is back in focus after the company highlighted solid growth in its Engineered Fastening and DEWALT businesses, supported by sustained aerospace demand and a completed cost-reduction program.

Recent price action reflects that story, with Stanley Black & Decker’s share price returning 21.55% over 90 days and 12.62% over 30 days, while the 1-year total shareholder return sits at 37.94% against a much weaker 5-year record.

If strong industry trends are on your radar, this is a good moment to look beyond Stanley Black & Decker and check out 32 robotics and automation stocks

So with Stanley Black & Decker stock trading at $84.62, an intrinsic value estimate that implies a 28.87% discount and a modest 7% gap to the average analyst target, are you looking at a genuine opportunity, or at a market that is already pricing in future growth?

Most Popular Narrative: 5.8% Undervalued

With Stanley Black & Decker stock at $84.62 against a widely followed fair value narrative of $89.87, the current pricing leaves a modest valuation gap and puts the focus squarely on execution.

The multi-year supply chain transformation nearing its final phase is delivering substantial recurring cost reductions, improved operational flexibility, and resilience to trade/tariff shocks. Management expects these initiatives to drive gross margin back to 35%+ by late 2026, supporting sustained improvements in net margins and earnings.

Want to see what is sitting behind that margin rebuild story, and how it ties revenue growth, earnings and valuation together? The narrative leans on a detailed earnings bridge, a specific view on long term margins and a future earnings multiple that differs from today. The tension between modest top line assumptions and much stronger profit growth is where the numbers get interesting.

Result: Fair Value of $89.87 (UNDERVALUED)

However, there is still real execution risk for Stanley Black & Decker if DIY and Outdoor demand stays soft, and if pricing actions continue to pressure volumes and margins.

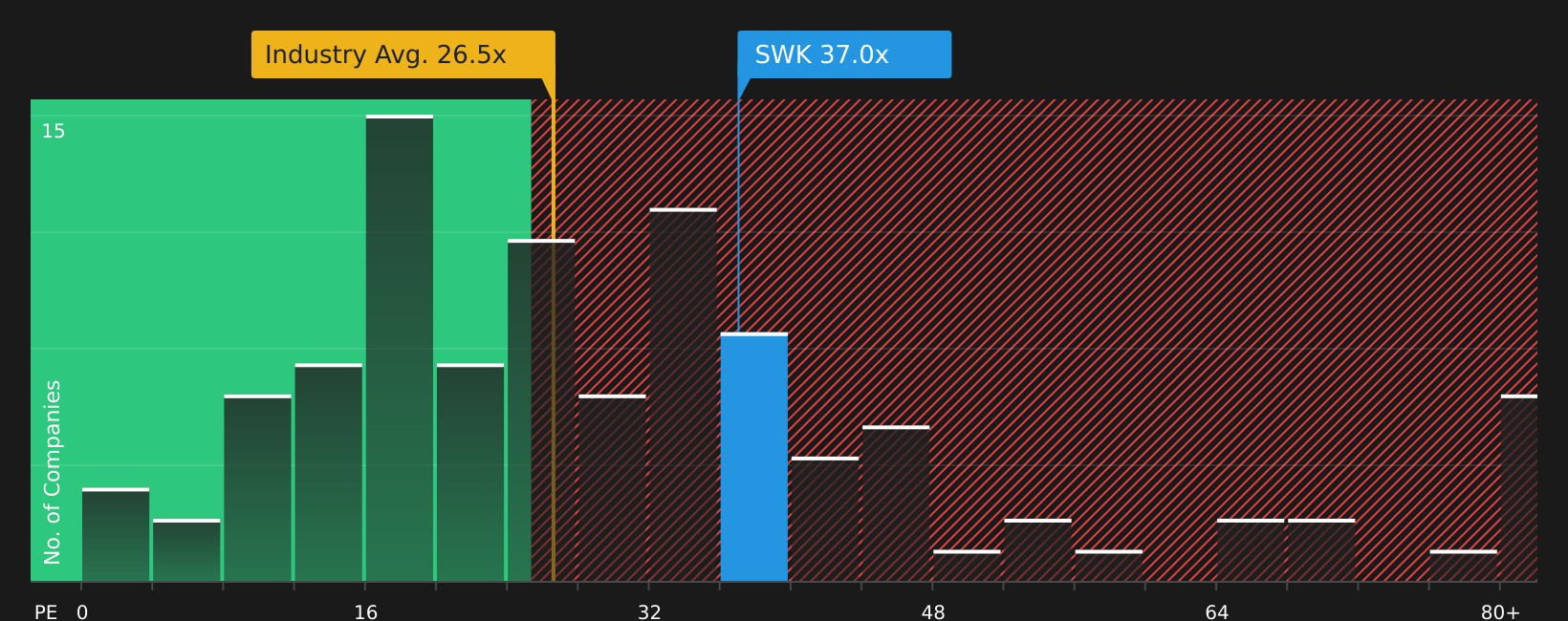

Another view on Stanley Black & Decker stock valuation

The fair value narrative for Stanley Black & Decker leans on earnings and cash flow, but the current P/E of 35.4x tells a different story. That is higher than the US Machinery industry at 27.5x and above peer averages at 27.1x, even though the fair ratio sits higher at 38.7x.

This mix of a discount to one fair value estimate and a premium to sector P/E levels leaves you weighing valuation risk against potential upside if the market ever moves closer to that fair ratio. Which reference point matters more for you when the next set of results lands?

Next Steps

With mixed signals across valuation, margins and end markets, where does Stanley Black & Decker really stand? Take a closer look at the underlying data, weigh the downside and upside, and decide how you feel about its 2 key rewards and 3 important warning signs

Looking for more investment ideas beyond Stanley Black & Decker?

If Stanley Black & Decker has sharpened your interest, do not stop here. Use the Simply Wall St Screener to uncover fresh opportunities that match your style.

- Target potential upside in quality companies trading below their implied value by scanning 44 high quality undervalued stocks, which pairs fundamentals with pricing gaps.

- Strengthen your watchlist with companies that prioritize financial resilience by running the solid balance sheet and fundamentals stocks screener (48 results) and focusing on sturdier balance sheets.

- Spot opportunities that others might be overlooking by filtering through a screener containing 20 high quality undiscovered gems built around strong fundamentals and quieter coverage.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.