Stocks to Watch | Meta Is Renting Out AI Compute — Yet Still Spending $10 Billion on New Data Centers. Is the AI "Overcapacity" Narrative Falling Apart?

Meta Platforms META | 0.00 | |

NVIDIA Corporation NVDA | 0.00 | |

CoreWeave CRWV | 0.00 | |

Goldman Sachs BDC, Inc GSBD | 0.00 | |

NASDAQ IXIC | 0.00 |

Just days after reports emerged that Meta Platforms(META.US) plans to commercialize its AI computing infrastructure, the company unveiled another $10 billion hyperscale data center project—its largest ever outside the United States. The combination has reignited one of the biggest debates in AI investing: if compute is truly becoming oversupplied, why is Meta still accelerating capacity expansion?

For many analysts, the answer is becoming clearer. Rather than signaling weakening demand, Meta's latest moves suggest the company is entering a new phase where AI infrastructure is no longer just a cost center, but an asset capable of generating recurring revenue while supporting another round of massive capital spending.

Meta's Expansion Suggests the AI Buildout Is Far From Over

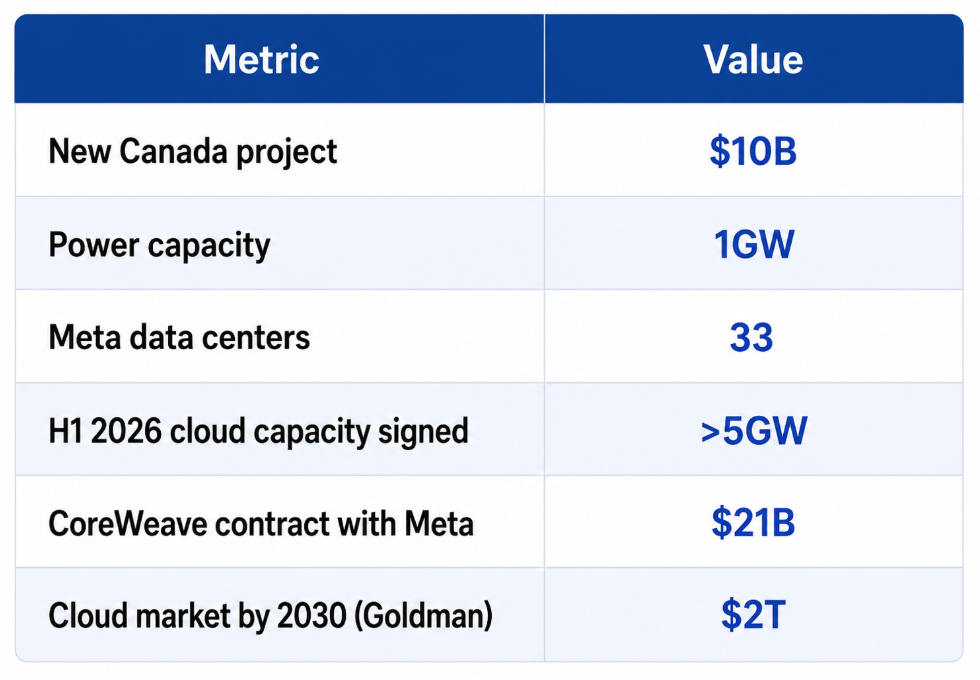

Meta announced plans to invest approximately $10 billion in a new hyperscale data center in Sturgeon County, Alberta, which will become the company's 33rd global data center and its largest facility outside the US, according to the company.

The campus is expected to deliver 1GW of power capacity—roughly equivalent to the electricity usage of 750,000 households—while creating 3,000 construction jobs and around 300 permanent positions.

The announcement comes only days after Bloomberg reported that Meta is exploring selling AI computing capacity and access to its AI models to external customers, a move widely interpreted as an attempt to monetize the enormous infrastructure it has built for internal AI development.

Rather than slowing investment after opening a new revenue channel, Meta appears to be expanding even more aggressively.

Research firm SemiAnalysis argues this directly contradicts the increasingly popular "AI overcapacity" narrative.

According to the firm, Meta has already contracted more than 5GW of cloud and hosted compute capacity during the first half of 2026, excluding its rapidly growing self-built infrastructure. SemiAnalysis expects Meta's infrastructure procurement to accelerate rather than slow, with 2027 capital expenditure projected to remain extraordinarily high.

Taken together, the data suggest Meta Platforms(META.US) is pursuing two strategies simultaneously: continuing to build new AI infrastructure while improving the utilization of existing assets.

Selling Compute Doesn't Mean Demand Is Weak—It Means Infrastructure Is Becoming Monetizable

The market's initial concern was straightforward: if Meta is renting out excess GPUs, perhaps it no longer needs all the computing power it has been buying.

Analysts increasingly disagree with that interpretation.

Meta CEO Mark Zuckerberg has previously said the company has the flexibility to lease portions of its computing resources externally, adding that this capability actually increases confidence in continuing to invest aggressively in AI infrastructure.

Everbright Securities believes the strategy transforms AI infrastructure from a pure cost center into an asset capable of generating cash flow. In the firm's view, monetizing surplus compute improves the economics of Meta's AI investments while helping finance future expansion.

More importantly, Everbright argues that the industry's primary bottleneck remains insufficient compute supply rather than excess capacity. From this perspective, leasing unused resources represents an optimization of existing infrastructure—not evidence that Meta is scaling back its long-term AI ambitions.

The brokerage notes, however, that investors have already priced in expectations for exceptionally strong capital expenditure. If compute commercialization begins generating meaningful returns, the likelihood of another major upward revision to Meta's CapEx guidance could become smaller, potentially creating short-term volatility around market expectations.

Subscribe to "The Trend Catcher Topic," tracking hottest sectors & technical breakouts in real time daily, accompanying you every US stock trading day.

Older GPUs Could Become Revenue-Generating Assets

Huatai Securities expects Meta to deploy next-generation AI chips—including NVIDIA Corporation(NVDA.US)'s GB-series and future Rubin architecture—primarily for frontier-model training, while reallocating older H-series GPU clusters toward AI inference workloads or external cloud leasing.

The firm believes this layered deployment strategy can significantly improve hardware utilization, allowing older infrastructure to continue generating returns instead of becoming stranded assets.

Huatai also notes that similar commercialization models have already shown early signs of viability at xAI, suggesting AI infrastructure could increasingly evolve into a recurring revenue business rather than a one-time capital investment.

Wall Street Is Repricing the AI Infrastructure Ecosystem

The market response highlights that investors are now debating who benefits from AI infrastructure commercialization, rather than whether AI demand itself is fading.

On July 8, Meta shares fell roughly 2% intraday, reflecting concerns that future capital spending may become more disciplined as monetization opportunities emerge. Meanwhile, CoreWeave(CRWV.US) gained nearly 8%, as investors weighed both the opportunities and competitive implications of an expanding AI cloud market.

Earlier, following Bloomberg's July 1 report that Meta was planning to sell AI compute and model access, Meta shares surged 8.6% in the following trading session, while CoreWeave dropped 14%, underscoring concerns that Meta could eventually compete with one of its own AI cloud providers.

The competitive dynamic is particularly noteworthy because Meta currently has a $21 billion AI cloud capacity agreement with CoreWeave extending through 2032. If Meta ultimately commercializes its own infrastructure at scale, it could gradually evolve from one of CoreWeave's largest customers into a direct competitor in parts of the AI cloud market.

At the same time, Goldman Sachs BDC, Inc(GSBD.US) Research estimates the global cloud computing market could generate $2 trillion in annual revenue by 2030, suggesting that the long-term opportunity may be large enough to support multiple infrastructure providers rather than a single winner.

The Debate Has Shifted

Meta's latest infrastructure announcement appears to strengthen a growing consensus among AI infrastructure bulls: commercializing compute does not necessarily imply compute demand has peaked.

Instead, analysts increasingly view compute leasing as a mechanism to improve return on invested capital while supporting even larger infrastructure expansion cycles.

If that thesis proves correct, the beneficiaries could extend across multiple segments of the AI value chain:

- GPU suppliers: Continued demand for next-generation AI accelerators such as NVIDIA Corporation(NVDA.US)'s GB-series and future Rubin architecture.

- Cloud infrastructure providers: Higher enterprise AI adoption may expand the overall addressable market despite increased competition.

- Power, cooling, networking and data-center infrastructure companies: Sustained hyperscale data-center construction would continue supporting demand across the physical AI infrastructure supply chain.

- CoreWeave(CRWV.US): Near-term sentiment may remain volatile as investors weigh the risks of future competition against continued demand for outsourced AI capacity.

Meta is no longer competing only in social media or open-source AI—it is increasingly entering the same commercial AI infrastructure arena dominated by Microsoft Corporation(MSFT.US) Azure, Amazon.com, Inc.(AMZN.US) AWS, Alphabet Inc. Class A(GOOGL.US) Cloud and Oracle Corporation(ORCL.US) Cloud.

For now, Meta's willingness to commit another $10 billion to AI infrastructure—even while preparing to monetize excess compute—suggests the company views commercialization not as an exit strategy, but as a way to finance the next phase of the global AI compute race.

Read more >>>

Stocks to Watch | Meta Spooks the Market: Buy the Dip in Semis or Revisit Mag7?