Stocks To Watch | Nvidia Earnings on Deck After the Bell! A Beat is Practically Guaranteed, But Wall Street is Focused on These 5 Questions

NVIDIA Corporation NVDA | 0.00 | |

Apple Inc. AAPL | 0.00 | |

Microsoft MSFT | 0.00 | |

Advanced Micro Devices, Inc. AMD | 0.00 | |

Broadcom Limited AVGO | 0.00 |

Subscribe to The Value Anchor Topic / The Trend Catcher Topic —unlock the full historical archive and never miss a weekly pick again.

NVIDIA Corporation(NVDA.US) is gearing up to deliver its fiscal first-quarter 2027 earnings after the market closes on May 20, and expectations are sky-high. According to S&P consensus estimates, the AI darling is projected to post Q1 revenue of $79.035 billion, up 79.37% year-over-year, alongside a staggering 127% surge in net income.

Historically, Nvidia has beaten EPS estimates for the past four consecutive quarters. The stock’s post-earnings move has averaged ±3.16%, carrying a 25% probability of a first-day gain.

While another top-and-bottom-line "beat" is widely seen as a foregone conclusion, Bank of America Securities analyst Vivek Arya and his team argue that the real market-moving catalysts lie in five specific questions management needs to answer on the earnings call.

Here is what Wall Street is watching:

1. Cash Returns: Will Nvidia stop being so "stingy"?

This is the core reason analysts believe Nvidia suffers from a chronic valuation discount.

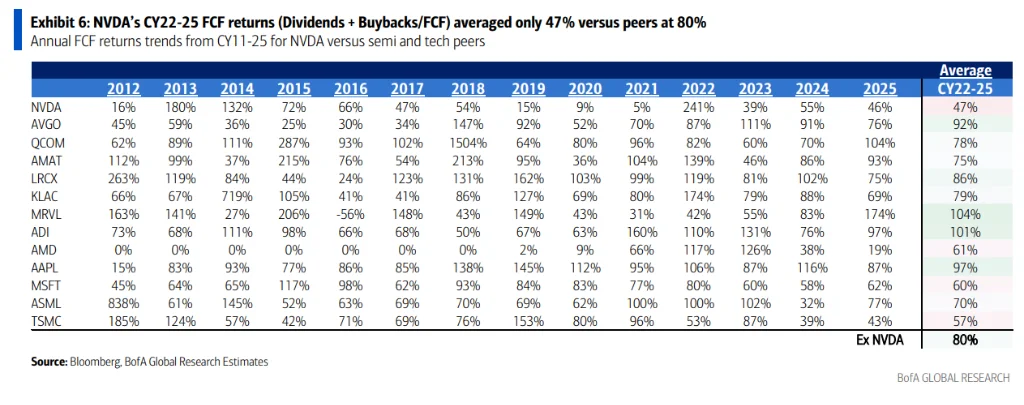

NVIDIA is currently the largest company in the S&P 500, commanding an 8.3% weighting—surpassing the historical peaks of both Apple Inc.(AAPL.US) (7.9%) and Microsoft(MSFT.US) (7.2%). Yet, the company’s shareholder returns are vastly disproportionate to its massive scale.

The numbers speak for themselves: From 2022 to 2025, Nvidia’s average free cash flow (FCF) return rate (dividends plus buybacks) was just 47%, compared to an industry average of 80%. Currently, Nvidia’s dividend yield is a meager 0.02%, trailing the 0.89% peer average.

So, where is the cash going? Analysts note that Nvidia has poured vast amounts of capital into its ecosystem—funding partners like OpenAI and Anthropic. These investments have sparked controversy, with some critics labeling them "circular financing," where Nvidia effectively lends money to customers who then use it to buy Nvidia chips.

How large is the valuation discount? Data shows that Nvidia's projected P/E ratios for 2026 and 2027 are 26 and 19, respectively, while the average for the other members of the "M7" is 49 and 42, respectively, representing a discount of nearly 50%.

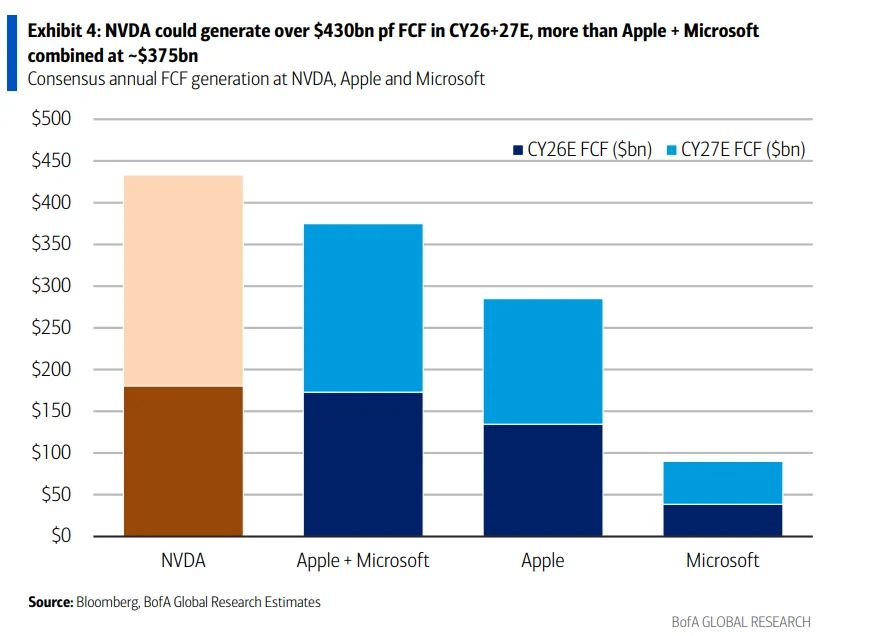

A more specific comparison is that analysts predict Nvidia's combined free cash flow for 2026 and 2027 will exceed $430 billion, higher than the combined $375 billion of Apple and Microsoft. However, Nvidia's market capitalization is approximately $5.46 trillion, about 28% lower than the combined $7.5 trillion of Apple Inc.(AAPL.US) and Microsoft(MSFT.US).

If Nvidia boosts its dividend and buyback programs, analysts believe it could attract long-term, yield-seeking funds, narrow its valuation gap, and dispel the "circular financing" narrative.

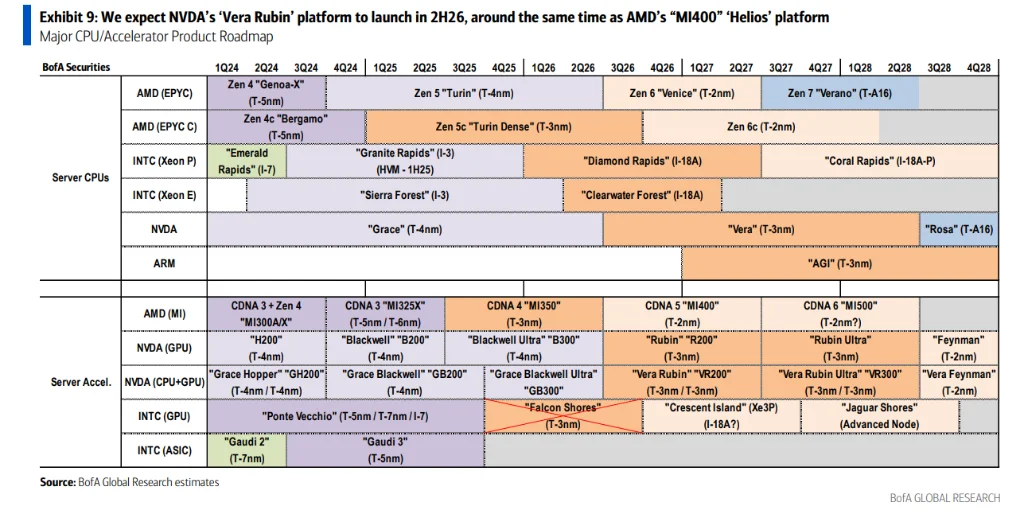

2. Vera Rubin: When will the next-gen chips arrive?

With the Blackwell series currently serving as Nvidia's flagship, the market wants to know when the next-generation Vera Rubin platform will officially scale.

BofA expects the rollout in the second half of 2026. Vera Rubin (codenamed R200) will utilize TSMC’s 3nm process and share the "Oberon" rack architecture with the Blackwell Ultra, allowing for a smooth transition with limited impact on gross margins.

Investors are also eager for an update on Nvidia’s previously teased "$1 trillion revenue forecast" for 2025-2027. Will management revise this to include unmodeled contributions from LPU (Language Processing Unit) racks, proprietary CPUs, and the Vera Rubin Ultra?

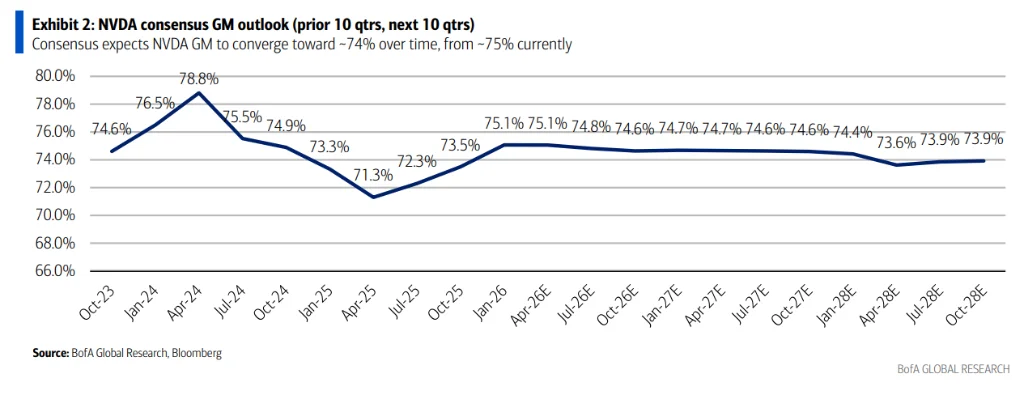

3. Gross Margins: Can the 75% defense line hold?

Gross margins remain a central pillar of Nvidia's premium valuation.

Analysts project that in the near term, margins will remain relatively stable. However, rising High-Bandwidth Memory (HBM) costs present a persistent headwind over the medium-to-long term.

Consensus estimates place Nvidia's gross margin squarely in the 74% to 75% range. BofA agrees with this baseline but emphasizes that any upside surprise here would be a major positive catalyst.

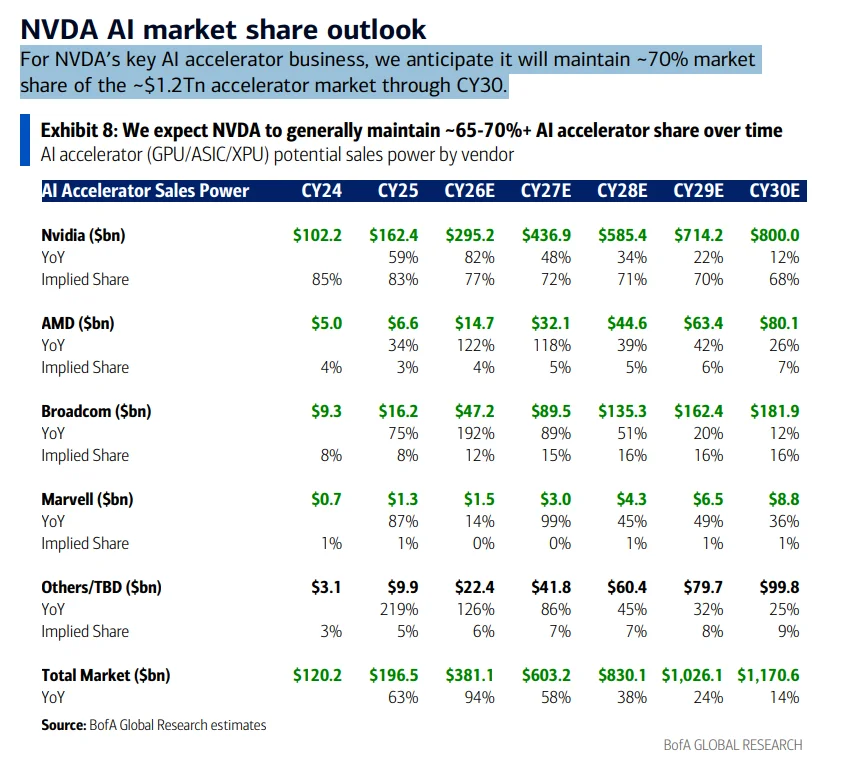

4. How will the AI Accelerator TAM be updated?

The Street is watching to see if Nvidia updates its Total Addressable Market (TAM) forecast to include three new growth drivers: LPU racks, the Vera CPU, and Vera Rubin Ultra.

By 2030, BofA estimates the broader AI accelerator market will reach $1.17 trillion, with Nvidia maintaining a dominant 68% to 70% market share.

Specifically, Nvidia's AI accelerator revenue is projected to grow from $102.2 billion in 2024 to $800 billion in 2030, while Advanced Micro Devices, Inc.(AMD.US)'s revenue is expected to grow from $5 billion to $80.1 billion and Broadcom Limited(AVGO.US)'s revenue from $9.3 billion to $181.9 billion during the same period.

5. Is the threat from Google TPU and competing CPUs overblown?

A recent market narrative suggests that as AI shifts toward the "Agentic AI" era, CPUs will become more important than GPUs, potentially eroding Nvidia's moat.

BofA categorically rejects this premise. First, Nvidia's proprietary "Vera CPU" will see new developments unveiled at Computex. Second, in currently deployed Blackwell and TPU clusters, the CPU-to-GPU ratio is already 1:2—contradicting the narrative that Agentic AI strictly requires vastly more CPUs.

The takeaway: Nvidia's stranglehold on the GPU/AI accelerator space is virtually unshakeable in the near term.

Subscribe to The Value Anchor Topic / The Trend Catcher Topic —unlock the full historical archive and never miss a weekly pick again.

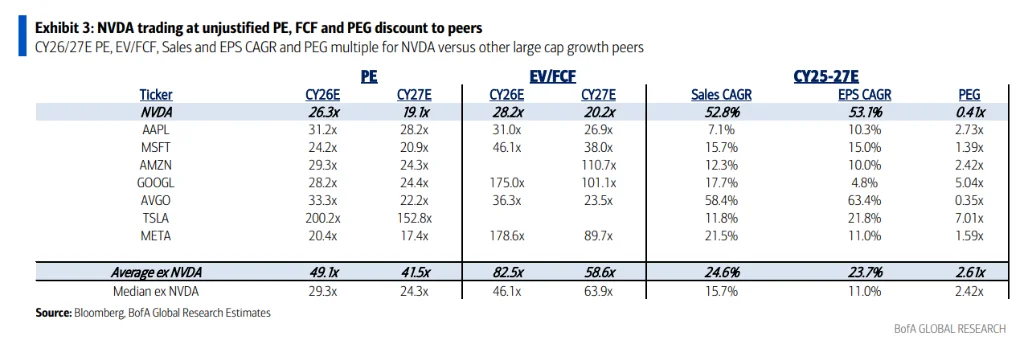

Valuation: A Tech Giant Trading at a "50% Discount"

BofA highlights a glaring valuation disconnect for Nvidia relative to its peers:

- P/E: Based on 2026/2027 estimates, Nvidia trades at 26x/19x forward earnings, while the rest of the Magnificent 7 averages 49x/42x—meaning Nvidia trades at a nearly 50% discount.

- EV/FCF: Nvidia sits at 28x/20x, while the Mag 7 averages 83x/59x (a >66% discount).

- PEG Ratio: Nvidia's PEG is a mere 0.41x, compared to the Mag 7 average of 2.61x and the broader S&P 500 at over 1.3x.

Bank of America maintains a "Buy" rating with a $320 price target, based on a 28x CY27 P/E (excluding cash), which sits at the lower end of its historical 25x-56x valuation range.

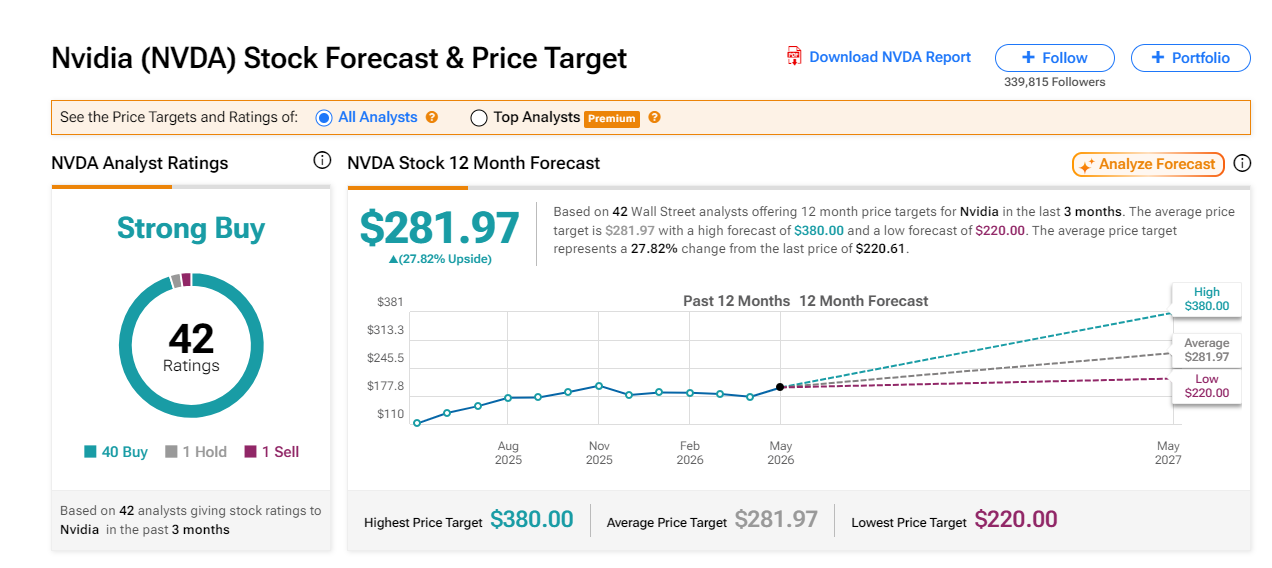

What Other Analysts Are Saying

According to TipRanks, over 90% of covering analysts maintain a "Buy" rating. The average Wall Street price target stands at $281.97, with a Street-high of $380 per share.

- Citi: Expects Q1 revenue to reach $80 billion, beating consensus by roughly $1.4 billion, driven by a stronger-than-expected B300 capacity ramp. For Q2, Citi forecasts an 11% sequential revenue increase to $89 billion.

- Wells Fargo: Significantly revised its Q1 estimates upward, raising its data center revenue outlook to $74.6 billion (+91% YoY). Analysts note that "gigawatt-scale" capacity expansion in AI infrastructure is the primary catalyst.

Sympathy Plays: Tracking Nvidia's Halo Effect

For investors looking beyond Nvidia, the earnings report is expected to create ripple effects across the broader tech ecosystem. Key sectors and related stocks to watch include:

- Chips: Advanced Micro Devices, Inc.(AMD.US), Taiwan Semiconductor Manufacturing Co., Ltd. Sponsored ADR(TSM.US), Arm Holdings(ARM.US), Qualcomm(QCOM.US), Broadcom Limited(AVGO.US), Marvell Technology(MRVL.US), Analog Devices(ADI.US)

- Semiconductor Equipment: Applied Materials(AMAT.US), Lam Research(LRCX.US), KLA(KLAC.US), Teradyne(TER.US), ASML Holding NV ADR(ASML.US)

- Utilities / Power: Vistra(VST.US), NRG Energy(NRG.US), First Solar(FSLR.US), Enphase Energy(ENPH.US)

- Servers: Dell Technologies(DELL.US), Super Micro Computer(SMCI.US)

- Software: Microsoft(MSFT.US), Alphabet A(GOOGL.US), Meta Platforms(META.US), Nutanix(NTNX.US), Palantir(PLTR.US)

- Data Storage: Everpure, Inc. Class A(PSTG.US), Western Digital(WDC.US), Seagate Technology(STX.US)

- Networking: Arista Networks(ANET.US), NetApp(NTAP.US)

- Electrical Components: Flex(FLEX.US), Amphenol(APH.US)

- Thermal Management / Cooling: VERTIV HOLDINGS LLC(VRT.US), nVent Electric(NVT.US)

- Copper / Fiber: Southern Copper(SCCO.US), Corning(GLW.US), Freeport-McMoRan, Inc.(FCX.US)

Leveraged and Inverse Nvidia ETFs: