Supermicro (SMCI) Stock Looks Cheap On Cash Flow Despite A 7x Return

Super Micro Computer, Inc. SMCI | 0.00 |

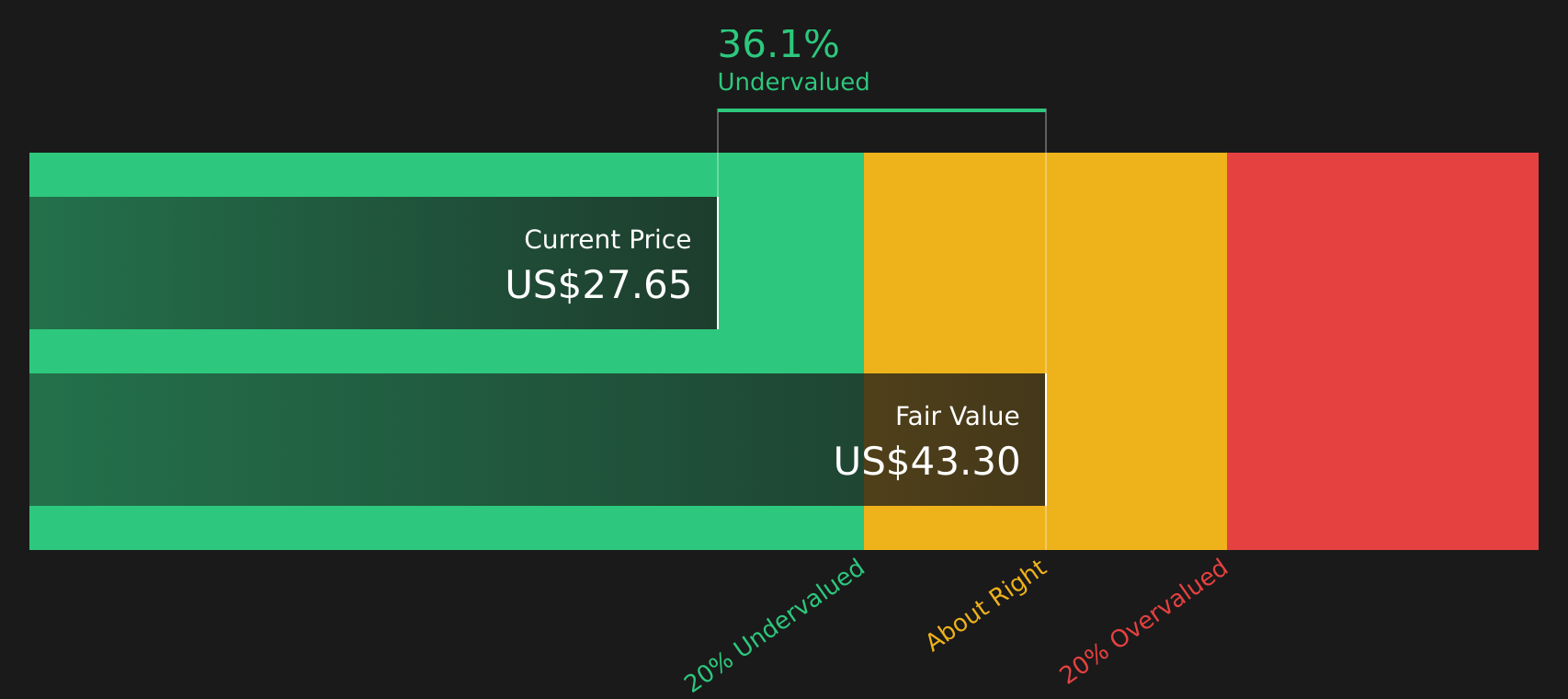

Super Micro Computer’s stock has swung sharply in recent months, yet current valuation checks point in the same direction. Both the Discounted Cash Flow (DCF) intrinsic value estimate and market multiples suggest the shares trade below what the fundamentals imply.

- Super Micro Computer has delivered a very large 5 year return of about 7x, which sets a high bar for what counts as attractive value today.

- Expectations around continued AI server demand and a sizable order backlog can support the long term cash flow story, while regulatory probes and capital raising needs may influence how investors price that growth.

- The broader valuation framework leans cheap, with Super Micro Computer screening as undervalued on 5 of 6 checks rather than looking fully priced.

For investors, the debate is whether the recent share price pullback has simply brought Super Micro Computer closer to its intrinsic value or left a meaningful margin between market price and what the underlying cash flows justify.

Does Super Micro Computer Look Undervalued on Cash Flow?

The Discounted Cash Flow (DCF) model estimates what Super Micro Computer’s future cash flows are worth in today’s dollars. The latest twelve month free cash flow shows a cash outflow of about $6.9b, and the model assumes that cash generation recovers and grows over time as current AI server demand and the order backlog convert into cash.

Based on those assumptions, the DCF points to an intrinsic value of about $43.30 per share in dollar terms, which sits roughly 32.3% above the current share price. On this basis, the stock appears undervalued according to this method. The recent $7b equity and equity linked financing to fund a sizable AI server backlog helps explain why the market is cautious even though the cash flow profile embedded in the DCF indicates a higher value.

On balance, the Discounted Cash Flow model suggests Super Micro Computer’s stock currently looks undervalued relative to its projected cash generation.

Our Discounted Cash Flow (DCF) analysis suggests Super Micro Computer is undervalued by 32.3%. Track this in your watchlist or portfolio, or discover 43 more high quality undervalued stocks.

Is Super Micro Computer a Bargain on Earnings?

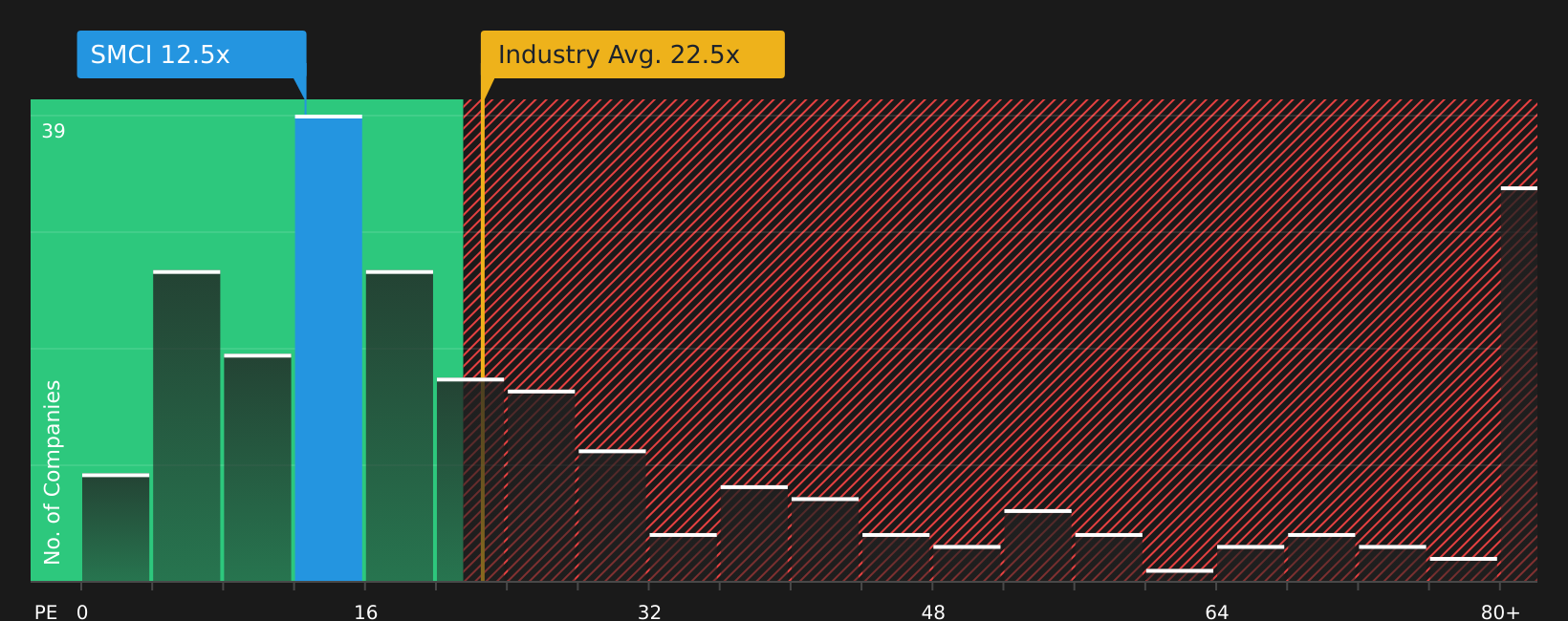

P/E is a useful yardstick for Super Micro Computer because the stock is closely tied to earnings from its AI server and data center hardware business. Right now Super Micro Computer trades on about 15.2x earnings, which sits below the broader Tech sector average of roughly 23.7x and also below a peer group average near 53.0x.

A tailored fair P/E ratio for Super Micro Computer, which incorporates its growth profile, margins, size and risk factors, comes out around 52.2x. That is higher than the current 15.2x, indicating that the market is assigning a substantial discount relative to what this framework suggests would be reasonable for the company. The gap can reflect investor concerns about regulatory investigations, capital intensity and execution on the large AI order backlog. Based on the raw numbers, earnings are being valued more cautiously than both the sector and the model indicate.

Overall, Super Micro Computer appears undervalued on its P/E multiple, with the current price reflecting a notable discount relative to both peers and the modelled fair ratio.

The Super Micro Computer Narrative: What Would Justify Today's Price?

Simply Wall St Narratives take the valuation puzzle around Super Micro Computer’s stock and link it directly to the specific assumptions on growth, margins and earnings that would need to hold for the shares to be worth materially more, or less, than today’s price. Rather than focusing on a single multiple or model output, each narrative lays out the underlying assumptions behind its view of fair value so you can compare them with actual results as they are reported. These narratives sit on Simply Wall St’s Community page.

Community views on Super Micro Computer sit far apart, with one camp focused on AI infrastructure upside and another fixated on margin and legal risk.

Bull case: 12% undervalued

"The accelerating global adoption of AI and analytics continues to drive demand for high-performance, scalable server and data center solutions, positioning Super Micro for strong multi-year revenue growth as enterprises and nations build out AI infrastructure, directly supporting projected revenue outperformance…"

Bear case: 20% overvalued

"One customer represented roughly 63% of Q2 FY2026 revenue…"

Do you think there's more to the story for Super Micro Computer? Head over to our Community to see what others are saying!

The Bottom Line

For Super Micro Computer, both the Discounted Cash Flow (DCF) intrinsic value estimate and the earnings multiple view currently point to the stock looking undervalued, even after a sharp share price move. The key question is whether the discount reflects temporary caution around funding needs, regulatory probes and the large AI server backlog, or a more lasting reset in how investors price that risk. From here, the crux of the debate is whether Super Micro Computer can convert its backlog and AI demand into durable cash generation without eroding margins or running into further legal or execution setbacks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.