The AI Infrastructure Stock Hiding Inside Nokia

Nokia Oyj Sponsored ADR NOK | 0.00 |

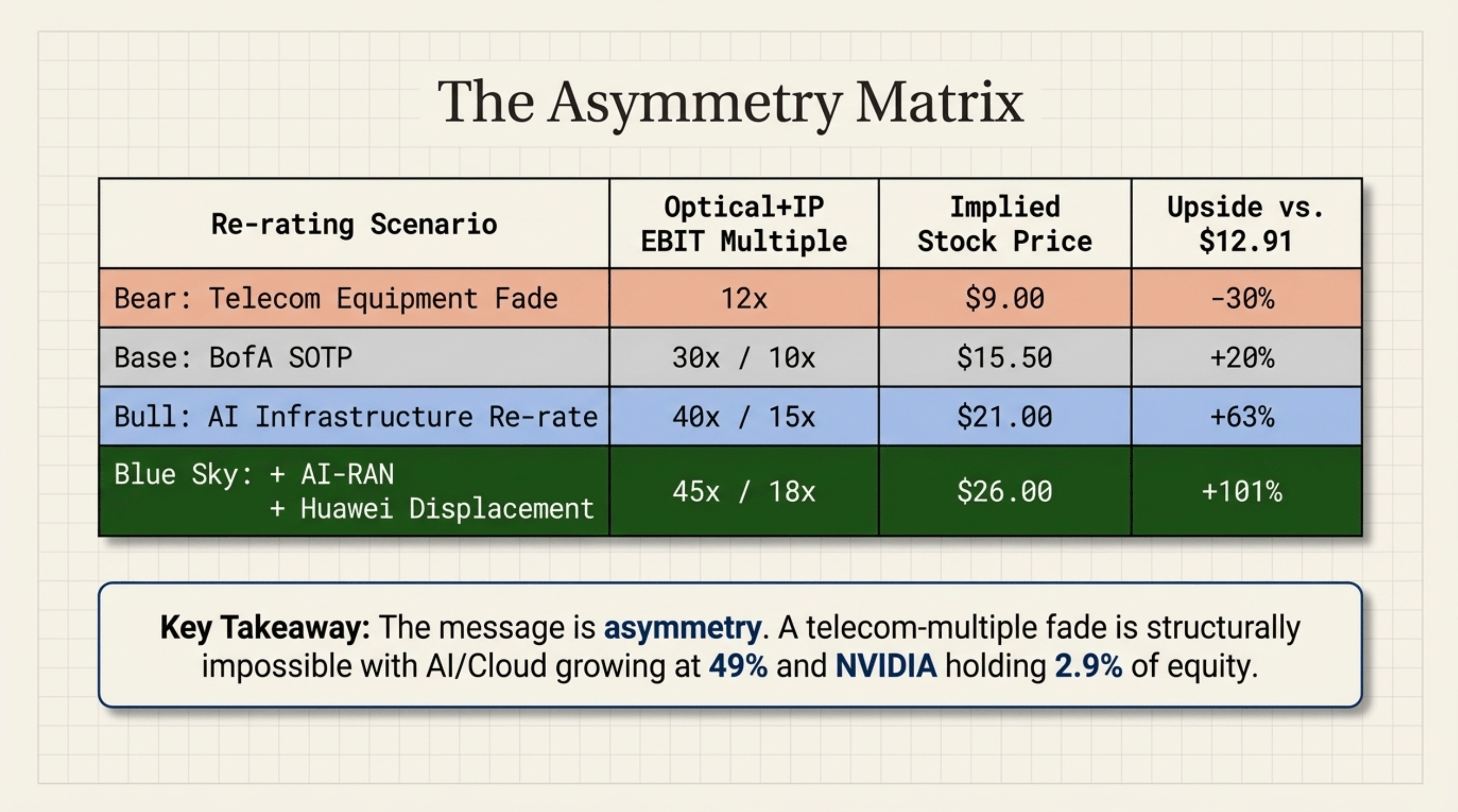

Sell-side EPS estimates are 13-15% too low. The defense business is modeled at zero. Three catalysts are converging.

This week’s Wolf Pick: Nokia (NOK)

Most people hear Nokia and think of the indestructible brick phone from 2004. Wall Street’s version isn’t much better. Until recently, consensus treated Nokia as a slow-moving European telecom equipment vendor trapped in the 5G spending hangover. That mental model just broke.

Nokia closed Friday at $13.30, a 16-year high. The stock is up roughly 166% over the past 12 months from a 52-week low of $4.00. Three things happened in the last six months that sell-side models haven’t fully absorbed, and they all point in the same direction: Nokia is re-rating from a low-multiple telecom laggard into a credible AI infrastructure name.

The NVIDIA signal and the orders that followed

In October 2025, NVIDIA committed $1 billion of its own balance sheet to Nokia at $6.01 per share. That’s not a strategic press release partnership. That’s real money at a specific price, anchoring Nokia inside NVIDIA’s AI-RAN initiative with T-Mobile for field trials at the end of this year.

Then Q1 2026 earnings landed on April 23 and reset the conversation. According to independent research shared with Wolf Financial, Nokia booked €1.0 billion of AI and Cloud orders in Q1 alone. AI and Cloud net sales grew 49% year over year. Gross margin expanded 320 basis points to 45.5%. Free cash flow jumped 40%. Network Infrastructure book-to-bill (the ratio of new orders to revenue shipped) ran at roughly 3x in AI and Cloud.

The number that matters most is one management revised on the earnings call. At their November Capital Markets Day, Nokia framed its AI and Cloud addressable market as growing at a 16% compound rate through 2028. Five months later, that figure was revised to 27%. The reason: hyperscaler capital expenditure expectations for 2026 jumped from $540 billion to over $700 billion. The entire bull case got 30% larger in five months.

Management raised segment guidance accordingly. Network Infrastructure growth went from 6-8% to 12-14%. Optical and IP Networks went from 10-12% to 18-20%. But they held the group-level operating profit guide flat at €2.0-2.5 billion. They raised the top of the funnel without raising the bottom. That’s the setup for a beat-and-raise pattern through the back half of the year.

The defense business nobody is modeling

On April 30, Anduril announced its 5G Comms Sentry Tower (CST), co-developed with Nokia Federal Solutions. The CST deploys in under three hours with no external power or infrastructure required, delivers 1+ Gbps throughput with sub-10 millisecond latency, and runs on Anduril’s Lattice software stack. It replaces three legacy options that all fail modern requirements: narrowband radios (too slow), satellite (too much latency), and commercial cellular (nonexistent in combat zones).

Research reviewed by Wolf Financial notes that Anduril already has over 400 Sentry towers deployed globally across U.S. Customs and Border Protection, Army, Navy, and allied programs. Every installation is a candidate for a 5G CST upgrade. Anduril’s own revenue trajectory tells you the scale: roughly $2.1 billion in 2025, projected at $4.3 billion in 2026, with a rumored $20 billion Army contract in negotiation.

Sell-side models have zero CST or defen se contribution in any Nokia forecast through 2028. Zero.

The pluggables ramp that sell-side isn’t running

The third angle is the one optical analysts are watching and everyone else is ignoring. Nokia’s coherent pluggables business (small modules that move data through fiber optic cables, replacing older, bulkier equipment) did roughly €151 million in 2025 revenue. That number is about to accelerate sharply.

Independent analysis reviewed by Wolf Financial projects Nokia’s pluggables revenue scaling from €281 million in 2026 to €627 million by 2028, a 49% compound growth rate. Nokia is one of only four companies globally with a credible next-generation roadmap for these modules, alongside Cisco, Marvell, and Ciena. After acquiring Infinera in early 2025, Nokia is the only vendor vertically integrated across the chip, the optics, and the system, with a domestic manufacturing facility in San Jose that no competitor can match.

The modeling disconnect is stark. Consensus still projects Nokia’s Optical and IP Networks segment at roughly 5% organic growth. Bottom-up analysis puts it closer to 15%. That gap puts 2026-2028 EPS estimates 13-15% below where they should be.

Where it trades and what to watch

Nokia trades at roughly 30x forward earnings. It’s no longer at telecom equipment multiples (Ericsson sits at 11-13x). But it’s nowhere near optical infrastructure multiples (Ciena at 77x, Arista at 47x). That middle ground is where the re-rating question lives.

Analyst price targets scattered across the board last week after Q1 earnings. Barclays, still rated Sell, hiked its target 54%. JPMorgan went to €12. Morgan Stanley to €11. Argus upgraded to Buy at $15. The dispersion itself tells you consensus is being dragged, not leading.

Q2 earnings (estimated July 21-23) should show pluggable revenue continuing to ramp. NVIDIA’s AI-RAN field trials with T-Mobile begin late 2026. Next-generation 1.6T pluggable samples ship in Q4. And the Anduril CST will start appearing in Anduril’s growth narrative throughout the year.

Risks worth noting: Q2 historically prints only 24-28% of full-year operating profit, so sequential moderation is normal. Supply constraints remain real, with 12-18 month optical lead times. And hyperscaler concentration risk is rising. These are pacing risks, not directional ones.

Thanks for reading! For more updates throughout the week, follow @WOLF_Financial on X.

Benzinga Disclaimer: This article is from an unpaid external contributor. It does not represent Benzinga’s reporting and has not been edited for content or accuracy.