Viasat (VSAT) Is Up 8.1% After Space Force Contract Win And Shelf Filing - Has The Bull Case Changed?

Viasat VSAT | 0.00 |

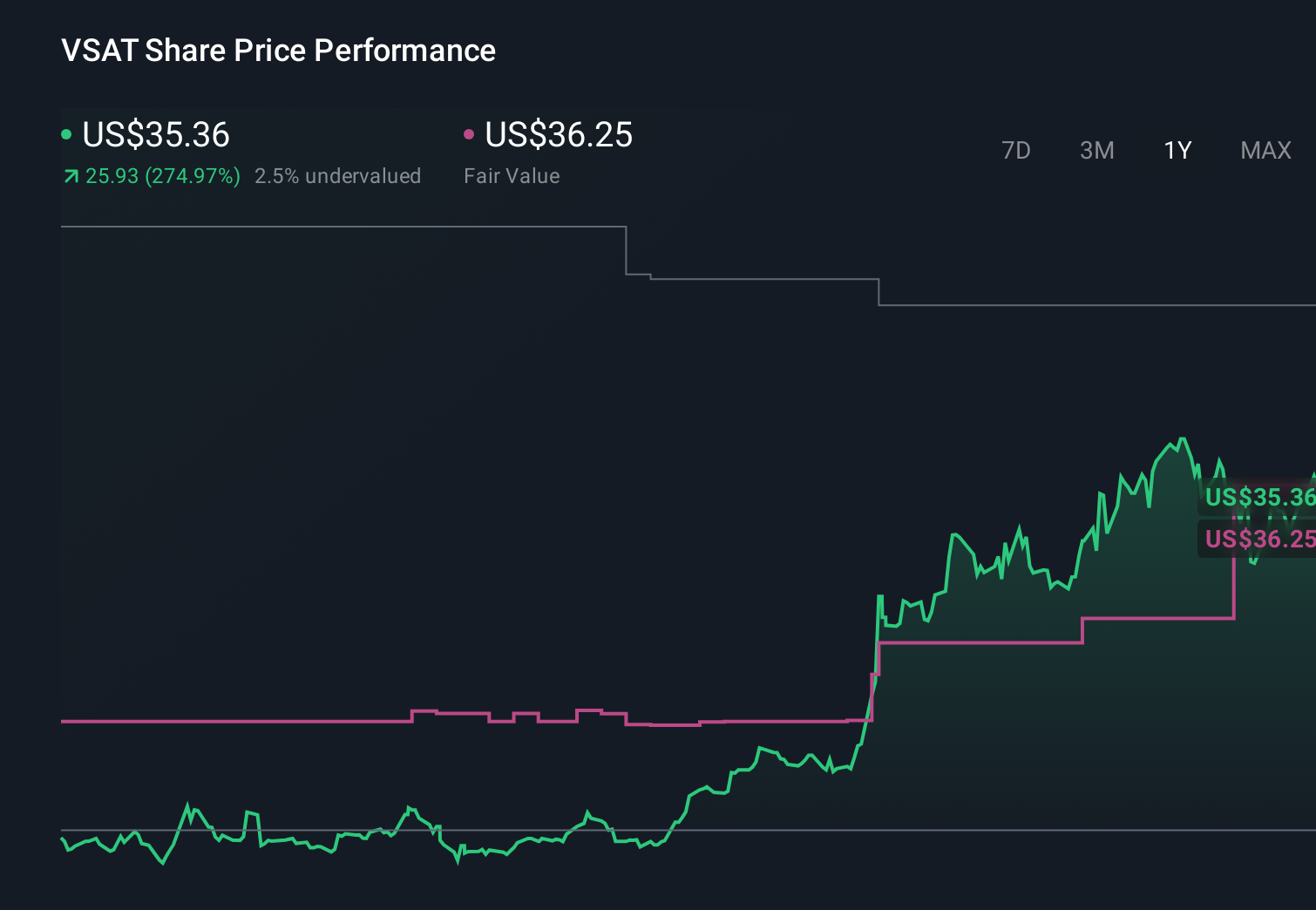

- In late May 2026, Viasat filed an omnibus shelf registration covering common and preferred stock, debt securities, depositary shares and warrants, shortly after reporting fourth-quarter revenue of US$1,171.29 million and net income of US$58.82 million.

- Alongside these filings, Viasat highlighted record new contract awards and a larger backlog, underpinned by a substantial U.S. Space Force Protected Tactical Satellite-Global contract win that supports its government and defense communications pipeline.

- With the major U.S. Space Force contract expanding Viasat’s backlog, we’ll now examine how this development may influence its investment narrative.

We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Viasat Investment Narrative Recap

To own Viasat, you need to believe its expanded satellite network and growing defense and government business can offset pressure in legacy broadband and capital-intensive projects. In the near term, the key catalyst is execution on large defense contracts like the new U.S. Space Force award, while the biggest risk remains heavy investment needs and leverage. The fresh omnibus shelf registration could matter if Viasat raises new equity or debt, but by itself the impact is not yet material.

The recent fourth quarter and full year 2026 earnings are central here. Viasat reported US$1,171.29 million in quarterly revenue, a swing to net income of US$58.82 million for the quarter, and modest full year revenue growth to US$4,640.28 million. Combined with record backlog and the Space Force contract, these results frame both the upside case around contract-driven visibility and the ongoing risk that high capital spending and integration demands continue to weigh on overall profitability.

But investors should also weigh the risk that rising competition and capital needs could still pressure Viasat’s cash flows and balance sheet...

Viasat's narrative projects $5.1 billion revenue and $557.4 million earnings by 2029. This requires 3.3% yearly revenue growth and about a $896 million earnings increase from -$339.0 million today.

Uncover how Viasat's forecasts yield a $51.14 fair value, a 37% downside to its current price.

Exploring Other Perspectives

The most cautious analysts paint a much harsher picture, expecting only about 3.3 percent annual revenue growth to roughly US$5.1 billion and continued losses, compared with the contract backlog and ViaSat 3 capacity story you need to believe in for the consensus view. These low-end forecasts highlight how far opinions can differ, and how news like the recent U.S. Space Force win might eventually shift either outlook.

Explore 8 other fair value estimates on Viasat - why the stock might be worth as much as 18% more than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Viasat research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Viasat research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Viasat's overall financial health at a glance.

Want Some Alternatives?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 12 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- The latest GPUs need a type of rare earth metal called Terbium and there are only 31 companies in the world exploring or producing it. Find the list for free.

- Find 46 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.