Will Stronger Earnings, Capital Returns, and AI Push Change Bank of America's (BAC) Narrative?

Bank of America Corp BAC | 0.00 |

- In mid-April 2026, Bank of America reported higher first-quarter net interest income of US$15,745 million and net income of US$8,584 million, alongside plans to redeem several billion dollars of senior notes and continue paying regular dividends across multiple preferred stock series.

- Together with an expanded share repurchase program and a public push to scale AI use across more than 90% of its workforce, these actions highlight how Bank of America is balancing capital returns, balance sheet management, and technology investment.

- Next, we’ll examine how this combination of stronger quarterly earnings and accelerated AI adoption could influence Bank of America’s existing investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 38 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Bank of America Investment Narrative Recap

To own Bank of America, you generally need to believe in a large, diversified bank that can turn disciplined lending, cost control and technology into steady earnings, even through economic swings. The latest quarter’s higher net interest income and net income support that narrative in the near term, while the biggest current risk still looks tied to how shifts in credit quality and funding costs could affect margins if market volatility picks up.

The most relevant recent announcement is Bank of America’s expanded share repurchase activity, with US$7,200 million of stock bought back in the first quarter of 2026. For investors focused on catalysts, this sits alongside ongoing AI investment as a key way management is trying to support per share earnings, even as competitive pressure for deposits and broader economic uncertainty remain in the background.

Yet at the same time, investors should be aware of how quickly credit costs could change if...

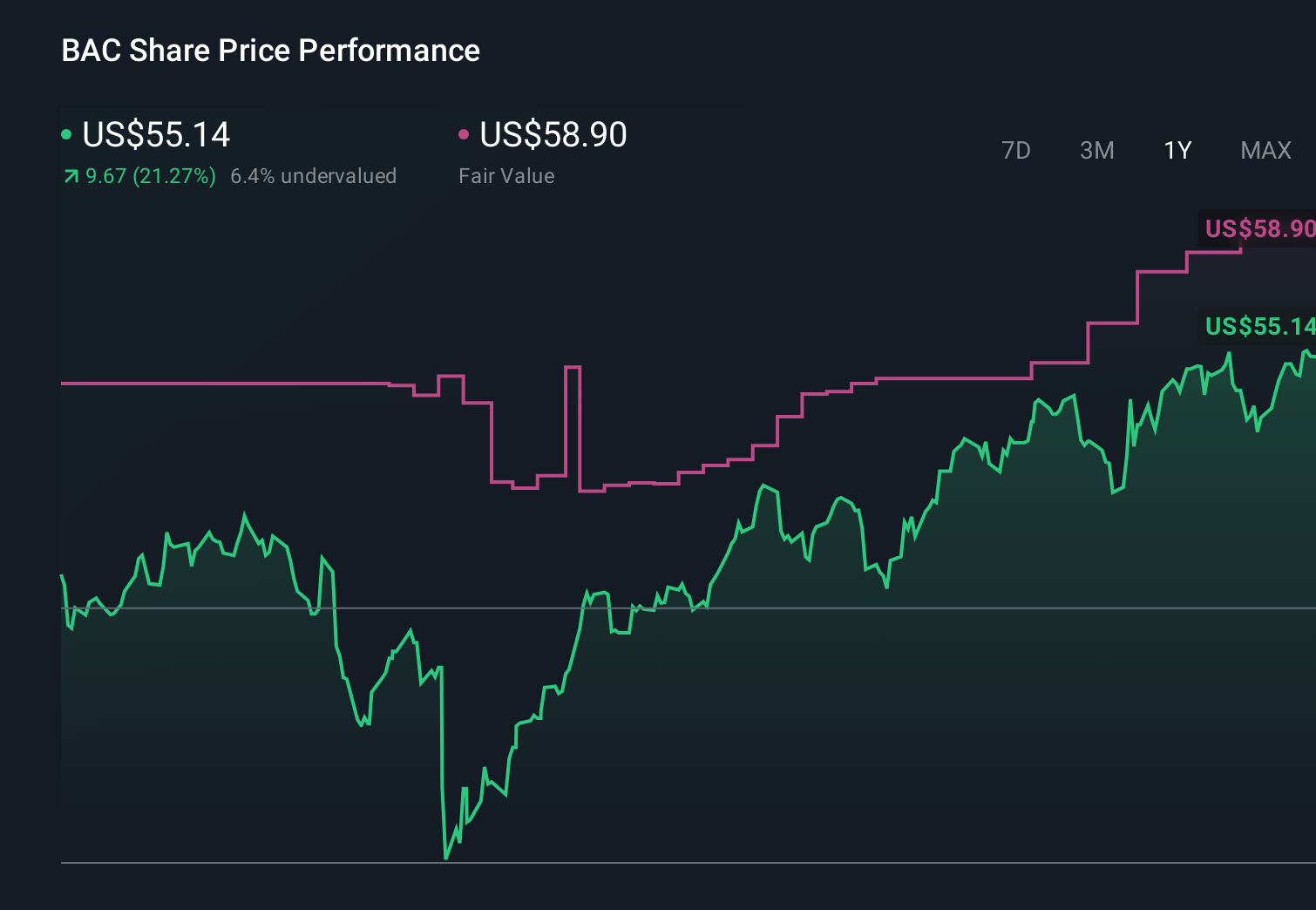

Bank of America's narrative projects $131.7 billion revenue and $36.6 billion earnings by 2029. This requires 7.0% yearly revenue growth and about a $7.5 billion earnings increase from $29.1 billion.

Uncover how Bank of America's forecasts yield a $60.42 fair value, a 12% upside to its current price.

Exploring Other Perspectives

Eleven members of the Simply Wall St Community currently see Bank of America’s fair value between US$52.22 and US$68.62, highlighting a wide spread of individual views. When you weigh those against the dependence on stable credit quality and funding costs discussed earlier, it underlines why many people compare several viewpoints before deciding how Bank of America might fit in their portfolio.

Explore 11 other fair value estimates on Bank of America - why the stock might be worth as much as 27% more than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Bank of America research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Bank of America research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Bank of America's overall financial health at a glance.

Interested In Other Possibilities?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- AI is about to change healthcare. These 37 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Find 60 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.